WEEKEND READING: International tuition fee-setting: why imitation is risky and what better looks like

This blog was kindly authored by Vincenzo Raimo, an independent international higher education consultant, and Patric Kirchner, Pricing & Commercial Excellence Partner at CIL Strategy Consultants.

In most sectors, pricing is treated as a strategic decision: it shapes demand, signals value and determines whether growth is sustainable. In UK higher education however, the setting of international tuition fees (and other non-regulated fees) too often feels like an annual cycle of cautious benchmarking and incremental change.

This piece draws on conversations with university leaders and builds on earlier HEPI blogs on pricing strategy, net revenue, and the proposed international student levy.

For readers who would like more background, see: ‘Beyond the margin: when might low net revenue in international student recruitment be justified?’ (HEPI, 14 April 2025); ‘Weekend Reading: How will universities respond to the 6 per cent international student levy?’ (HEPI, 4 October 2025); and ‘Pricing strategy: the missing lever in university sustainability’ (HEPI, 12 November 2025).

A useful parallel from grocery (imperfect, but instructive)

Pricing research describes a well‑documented form of ‘herd’ behaviour: organisations set prices primarily by reference to competitors, rather than by reference to strategy, value and the outcomes they are trying to achieve. It is easy to see why: competitor moves are visible, whereas your own value proposition can feel contested and harder to quantify.

A useful parallel comes from the UK grocery industry. As Aldi and Lidl grew market share, the larger supermarkets responded with highly visible value signals, for example, ‘Aldi Price Match’ ranges, loyalty-linked pricing and expanded own-brand value tiers.

Higher education is not retail, and the analogy is imperfect, but the underlying dynamic is familiar: when customers become more price-sensitive, organisations often end up managing a widening gap between a headline offer (the shelf price) and what customers actually pay (after targeted discounts and promotions).

In international student recruitment, the equivalent risk is that institutions focus on the published fee as the primary reference point, while the realised price is increasingly shaped by scholarships, discounts and mid-cycle incentives. The strategic question then becomes not only what the headline fee says about positioning, but whether the institution can see – and actively manage – the net fee, the acquisition cost, and the resulting contribution with enough confidence to make deliberate choices rather than reactive ones.

International tuition fees: convergence without confidence

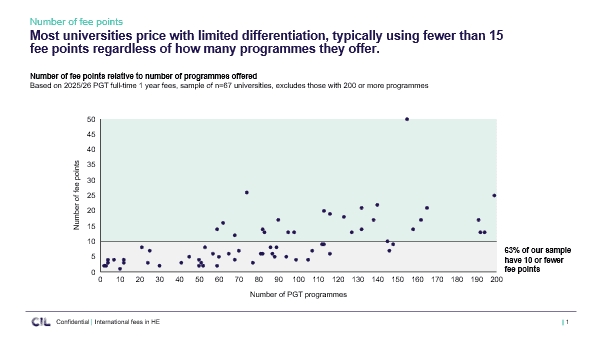

A simple review of published fee tables for one‑year full‑time taught postgraduate programmes reveals a set of consistent features:

- Very few published fee points across highly diverse subject portfolios (often just a small number of ‘bands’).

- Tight clustering of fees within perceived peer or ranking groups.

- Limited differentiation by demand, outcomes or delivery costs.

- Frequent use of scholarships and discounts to correct short‑term recruitment shortfalls (sometimes introduced mid‑cycle).

From a pricing perspective, this is unusual. In most sectors, organisations offering hundreds of differentiated products would not price them within such a narrow range. Yet in universities, where programmes differ markedly in cost, demand and student outcomes, limited fee banding is normal practice.

What we are hearing from institutions

Our pricing and cost-of-acquisition conversations with universities over the past few months suggest the challenge is not only what to charge, but whether institutions have the information and governance mechanisms to make pricing decisions confidently. A few recurring themes stand out:

- Cost of acquisition is rising, particularly agent commission, and the direction of travel is rarely modelled explicitly alongside fee decisions.

- Many institutions have limited internal visibility of cost of acquisition because data sits across systems (CRM, admissions, finance, marketing) with weak analytics capacity to join it up.

- Competitor intelligence is often based on published list fees that may be out of date, incomplete, or poor proxies for net price after scholarships and in-market discounting.

- Fee banding can become a constraint: when a university has only a small number of price points, it has fewer options to respond to changing demand without resorting to blanket discounts.

- Mid-cycle discounting (automatic scholarships, fee waivers, time-limited incentives) can be disruptive: it may secure volume, but can also reset expectations, confuse partners, and erode trust if not handled transparently.

- For institutions in England, uncertainty about how to respond to the international student levy, and a ‘wait and see’ tendency that delays decisions.

Why ‘list price’ still matters

Universities rightly point out that scholarships and other support create differentiation beneath the published fee. But the published tuition fee still matters: it anchors perceptions of value, provides transparency, and sets the reference point from which support, services and future outcomes are judged by students, families, agents, sponsors and policymakers.

If list price is set largely by imitation, downstream adjustments tend to become reactive too. That makes it harder to defend value, harder to explain decisions internally, and harder for governing bodies to understand the true net price by market, channel and programme.

The risk: headline prices rise while realised fees stagnate (or fall)

One hidden risk in international fee-setting is the growing gap between headline (published) fees and realised (net) fees.

In many institutions, published international fees have continued to increase year on year, and often by more than inflation. On paper, that can look like healthy pricing discipline. But the real pressure is on the net fee actually paid once scholarships, discounts, agent-funded incentives, and in-cycle automatic fee reductions are taken into account.

The result is a quiet squeeze on net contribution: committees can see a rising list price and assume the margin position is strengthening, while in practice the institution is standing still at best, or giving ground through untracked or poorly understood discounting. This is compounded by the fact that competitor comparisons typically rely on published fees, not on what students actually pay.

When realised fees stagnate or decline, the institutional response is predictable: more volume is needed to hold income and protect fixed-cost recovery. But that can be a risky strategy in a more volatile market, particularly if acquisition costs are rising at the same time. This is why visibility of realised net fees and full cost of acquisition is now central to effective pricing decisions rather than an optional ‘nice to have’.Top of FormBottom of Form

Why imitation feels safe – and why it is not

In our conversations, the most common justification for holding or reducing net fees is simply: “the competition”. Pricing responsibility is externalised, even though not everyone can follow competitors at the same time, and governance becomes harder.

Peer benchmarking is understandable: it provides a sense-check and can protect institutions from obvious missteps. But when benchmarking becomes the strategy, confidence erodes. Universities may assume others have better data or a clearer rationale, when in practice many are working from the same limited signals and datasets.

What might more mature pricing look like in higher education?

More mature approaches to setting non‑regulated fees tend to share a small number of features:

- Pricing is anchored in strategy: institutions are explicit about what they are trying to achieve (income, diversification, quality, scale, or a deliberate balance).

- Programmes are not treated as equal: differences in demand, outcomes, delivery costs and strategic importance are reflected in decisions.

- Fees and cost of acquisition are considered together: scholarships, discounts, commission and marketing spend are treated as part of a single system, with visibility of net tuition by market, channel and programme.

- Pricing is treated as a capability, not an annual exercise: clear governance, reliable data and analytical capacity underpin confidence and consistency.

None of this requires universities to ignore competitors. But it does require leaders to decide when to follow and when to differentiate, and to be explicit about what good looks like for their own strategy and risk appetite.

A new era of pricing risk

UK higher education is entering a period in which pricing decisions will carry greater weight: international markets look more price‑sensitive; the cost of acquisition is rising; margins are under pressure; and growth through volume alone is increasingly constrained, not least because policy change could tighten economics further.

A further complication, for universities in England, is the international student levy. When introduced, it will add a new, visible cost line to every international enrolment and will raise strategic choices: whether to absorb the levy (and accept lower net contribution), pass it on through higher fees, offset it through changes to scholarships/discounting, redesign the channel mix and offer so that overall net revenue is protected, or in some cases, step back from active recruitment in markets/programmes where the economics no longer clear an acceptable net-contribution threshold. Whatever route an institution takes, the levy increases the value of having timely, integrated visibility of acquisition costs and realised net fees.

Questions for senior teams and governing bodies

If pricing is to move from an annual routine to a strategic lever, a few practical questions can help focus discussion:

- Do we have a clear view of net tuition income by market, channel and programme (after scholarships/discounts and commissions)?

- Do we understand our total cost of acquisition, and how it is changing (including agent fees, marketing, in-country resource and institutional overhead)?

- Which decisions are ‘strategic’ (set centrally) and which are ‘tactical’ (managed in-cycle), and who has authority to approve discounting?

- Is our competitor intelligence robust and current, and does it include an informed view of net pricing, not just published list fees?

- Are our fee bands and scholarship rules helping us to deliver our objectives or constraining us into blanket discounts?

The lesson from other sectors is not that higher education should commercialise. It is that pricing without intent produces outcomes no one actively chooses. At a time of tighter margins and greater scrutiny, universities that can link fees, cost of acquisition and strategic objectives will be better placed to protect quality, access and long‑term sustainability.

What to do now

The invitation is simple: treat international pricing as an executive-level strategic lever, not an annual administrative exercise. Build the minimum evidence base (realised net fee by programme and market; full cost of acquisition by channel; and sensitivity to discounts, commissions and policy changes such as the levy). Then make explicit choices about what your institution is optimising for: growth, diversification, access, quality, risk reduction, or net contribution, and align fee-setting, scholarships and recruitment investment accordingly. If we continue to rely on published competitor fees, partial data and mid-cycle reactions, we should not be surprised when outcomes feel increasingly volatile.

For governing bodies, the practical test is whether you can answer, with confidence:

What did an additional international student really contribute last year once discounts, commissions, marketing and support costs are included, and for those in England, how would that change under the levy?”

If the answer is unclear, prioritising better data and sharper decision processes is not a ‘nice to have’; it is now a core part of financial stewardship.

Comments

Add comment