How is the higher education sector faring at the end of 2025/26 (And what 10 points does Andy Burnham need to know about it?)

This blog was authored by Nick Hillman, CEO of HEPI.

The piece is a revised version of a report written originally to inform Council members at the University of Buckingham for a strategic away day.

1. Political positioning

As a Post-16 Education and Skills White Paper appeared in October 2025, it might be expected that the English tertiary education sector would be talking now about nothing other than implementation of a clear set of official proposals. However, the White Paper has not yet left the mark expected, perhaps because many of the hard plans for higher education were generally based on previous announcements, such as the Lifelong Learning Entitlement, but also because the Department for Education has not gained a spot for new primary legislation in the current parliamentary session.

Meanwhile, the other political parties have offered only scant alternative prospectuses for England. These include slashing the number of degree places (as with the Conservatives and Reform UK) and abolishing tuition fees (as with the Green Party). The level of detail in such policies is so vague that they resemble nothing much more than a puff of smoke, although – to be fair – the next Westminster election could still be years away.

In Scotland, the continuation of the SNP Government after the May 2026 election to the Scottish Parliament makes major changes less likely (despite the Future Funding Framework review supported by the Government and Universities Scotland). In Wales, the new Plaid Cymru Government could make it more costly for Welsh-domiciled people to access higher education elsewhere in the UK.

It is plausible that the forthcoming change of Prime Minister could lead to a distinctly new direction of travel for higher education policy in England, with knock-on consequences for funding in other parts of the UK. Andy Burnham and other senior Labour figures who could take on prominent roles in any new administration have been associated with quite well-developed policies on education: Andy Burnham has been a firm advocate for technical education; Wes Streeting has previously backed a graduate tax; and Ed Miliband pushed for much lower tuition fees when he was the Leader of the Opposition. But the extent, let alone direction, of any future change remains far from certain, not least because of the pressing challenges in other policy areas, including the NHS, defence and the economy.

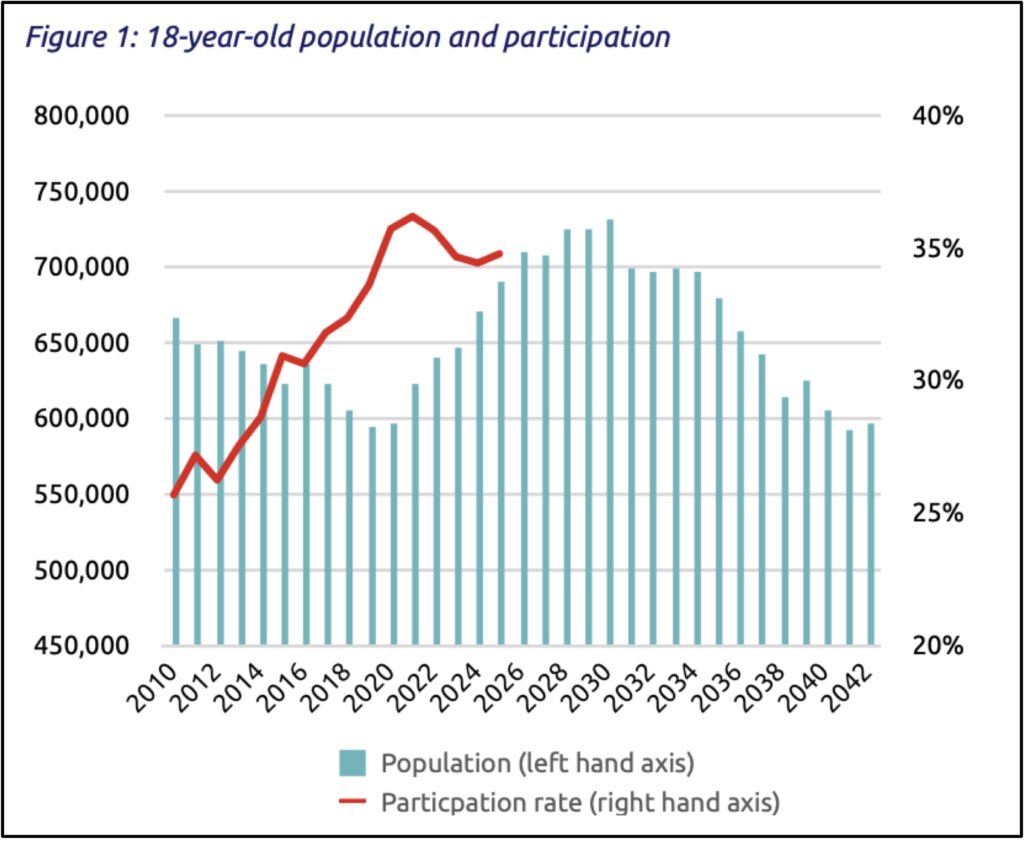

2. Demographics and demand

The end of this decade is the absolute high point for the gradually rising number of school leavers, reflecting birthrates in the early 2010s. However, there was an unexpectedly large surge in demand for higher education around the time of COVID, when the labour market was tough and young people wanted to avoid being locked down with their families. This was then followed by a modest slump in demand for a couple of years afterwards. In other words, trends in demand have not always closely tracked the growing number of young people but reflect other factors too.

Demand now seems to be rising again, but it could yet prove to be soft: for example, no one knows for certain if the noise around student loans in the media from January 2026 onwards will affect how many new students actually enrol in the autumn. Moreover, whether the total cake gets slightly bigger, stays the same or reduces in size, the more selective universities (especially Russell Group members) are likely to continue hoovering up the crumbs.

Most notably, after 2030 the number of school leavers falls dramatically, likely heralding a crisis worse than the current one, especially for ‘recruiting’ as opposed to ‘selective’ institutions.

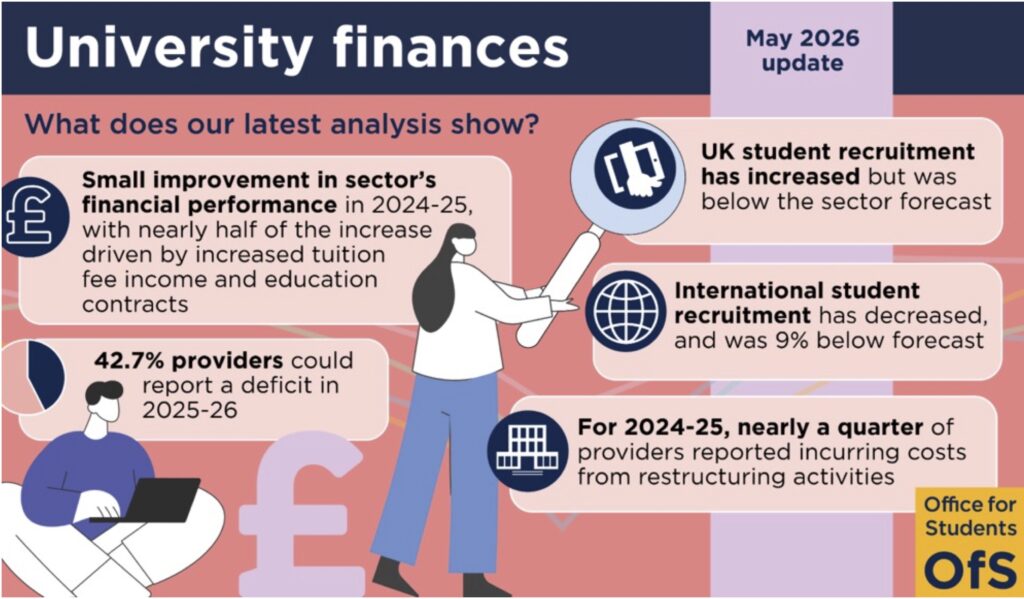

3. Financial position of institutions

The overall financial position of the sector’s c.150 universities remains dire, even if only one (the University of Dundee) is being publicly bailed out and even if only a tiny handful of institutions have so far resorted to mergers to help keep them afloat.

The current and promised future rises in the tuition fee / loan caps for home undergraduates will only keep current fee levels in line with inflation at best, forgoing the opportunity to play catch up, while other changes like the forthcoming International Student Levy are set to add yet more costs.

The dicier higher education institutions on the Office for Students’ Register tend to be found among the 250+ higher education providers that have not yet secured the right to call themselves a ‘university’. But redundancies and reforms have still been needed to keep the wolves from the door at many universities. If any university were to fall over, the risk of wider contagion (a domino effect) is real.

Recent upset in the independent school sector is instructive here, as the legal status of independent schools and autonomous universities is similar. When an institution leaves it too late to talk to others about future options, potential suitors lose interest as it can look like there is too little meaningful left to save.

While stronger higher education providers continue to make a surplus, even if not at the c.10% level they would ideally like, others can currently only dream of this. Some feel there must be ‘light at the end of the tunnel’ for the higher education sector as a whole but the source of any such light is not yet clear and recent history suggests there is a tendency for institutions to be overly optimistic in their projections.

The Office for Students’ remaining Strategic Priorities Grant (what used to be called the Teaching Grant), which supplements higher education institutions’ incomes for some teaching, is expected to be cut (again) in coming weeks. It is also expected that Ministers will soon seek to introduce minimum entry criteria to bar less-qualified applicants (such as those without a good grade in an English GCSE) from higher education, thereby imposing more control over the number of students and the financial exposure of taxpayers to unpaid student loans.

4. Financial position of students

If anything, the financial position of students is more dire than the financial position of higher education institutions. Maintenance support has not kept up with inflation, let alone the true cost of being a student. Loughborough University’s pre-eminent Centre for Research in Social Policy team have calculated for HEPI / TechnologyOne that a student needs over £20k each year if they are to play a full part in university life. Yet the maximum maintenance loan is more like £10k and even that is only available to those from lower-income households (on below £25k per annum, a level that has been fixed since the early days of Gordon Brown’s premiership).

The result can be seen very clearly in HEPI’s own data: over two-thirds of full-time undergraduates now work in paid employment during term-time (up from one-third five years ago), over half of students miss an average of one-third of their in-person contact hours and independent learning hours are materially down. The Treasury have been known to deny there is a problem, even claiming fewer students are working, but this claim rests on Labour Force Survey data that is not only unreliable for students but which also pre-dates COVID, thereby missing the post-pandemic period of high inflation that hit students so hard.

When the Milburn review of the NEET (Not in Education, Employment or Training) crisis was published in May 2026, many people were keen to focus on the small proportion of graduates who are economically inactive. But the more important issue when it comes to higher education is whether the large number of full-time students taking jobs, including during term-time, is worsening the NEET crisis.

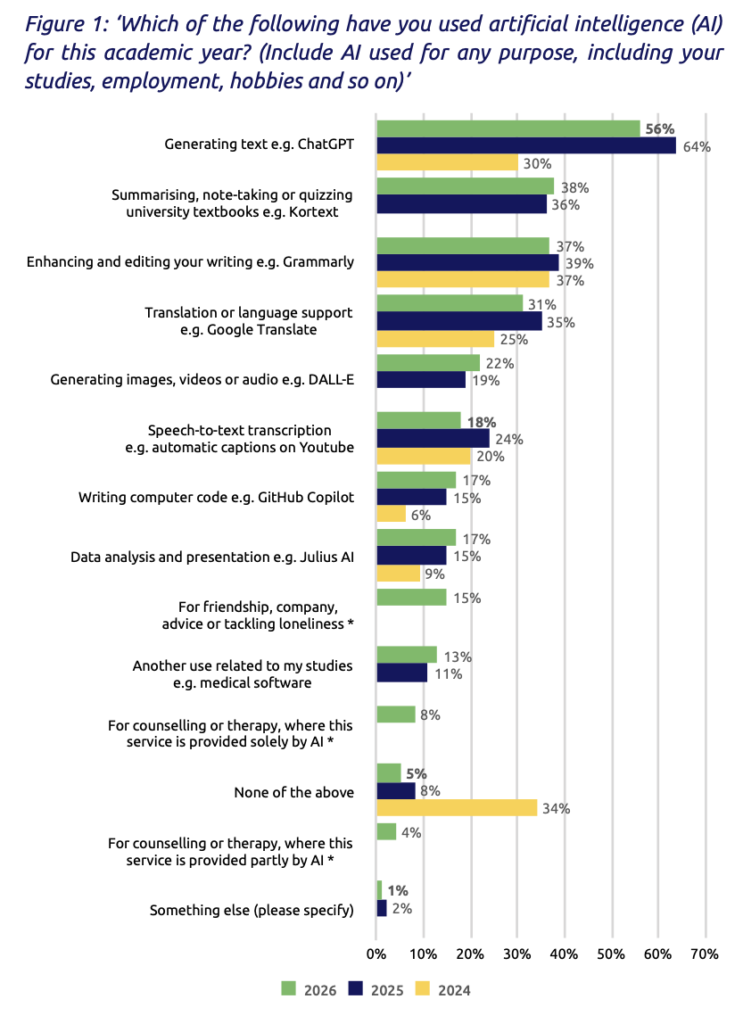

5. AI

AI is ubiquitous among students. Only a tiny handful (5%) have resisted its blandishments, possibly because of environmental and ethical concerns. There is a huge appetite for events and articles on what AI means for higher education and education more generally as well as what is means for the labour market.

This is not surprising because it remains uncertain which part of universities will be most affected first. Will it be professional services, assessment and evaluation of students’ work or pedagogy? How can a university educate all its students equally when some students have access to much better technology than others? What does AI mean for the supply of entry-level graduate jobs?

No one seems to know for certain how it will all play out and universities are struggling even to decide if their AI policies should be focused on detection, enforcement and penalties or trusting students to use the new technology in ways that will make them smarter and more efficient. Any university, wherever it is situated, that successfully carves itself out a leading niche here will become world famous.

6. Position of the Office for Students (OfS)

On the one hand, the Office for Students looks in a precarious position since it lost the legal action brought against it by the University of Sussex. But the organisation has a new-ish and hands-on Chair with experience of leading a large institution very successfully (Edward Peck, formerly of Nottingham Trent University). Baroness Jacqui Smith, the Minister for Skills, was fairly bullish about the OfS’s future when appearing at the HEPI Annual Conference on 11 June 2026. Meanwhile, the incoming permanent CEOs, Polly Payne and Ruth Hannant, are very knowledgeable about higher education, having worked on the current legal framework, as well as the broader realities of public policy, having worked in senior roles at the Treasury and other Government Departments.

Any institution doing something differently or which has had particularly good or bad experiences should engage with the OfS’s new leaders forthwith. After all, while many people might like to see the OfS replaced, it seems highly unlikely that any government would make this an urgent priority and, given a market-driven system needs a market regulator, it is not clear how different a replacement would look unless there were oodles of public money to fund higher education differently.

7. Shape and size of sector

Some of those who are known for complaining about the state of modern higher education ascribe many of today’s challenges to the growth in student choice after 2012. Professor Stefan Collini, for example, recently peered out of his ivory tower to bemoan the state of English higher education via the pages of the London Review of Books. On the other hand, many of those who have looked closely at the whole sector tend to think the core objective of the Higher Education and Research Act (2017) to diversify the provision of higher education in the interests of student choice has not worked out to the degree once envisaged.

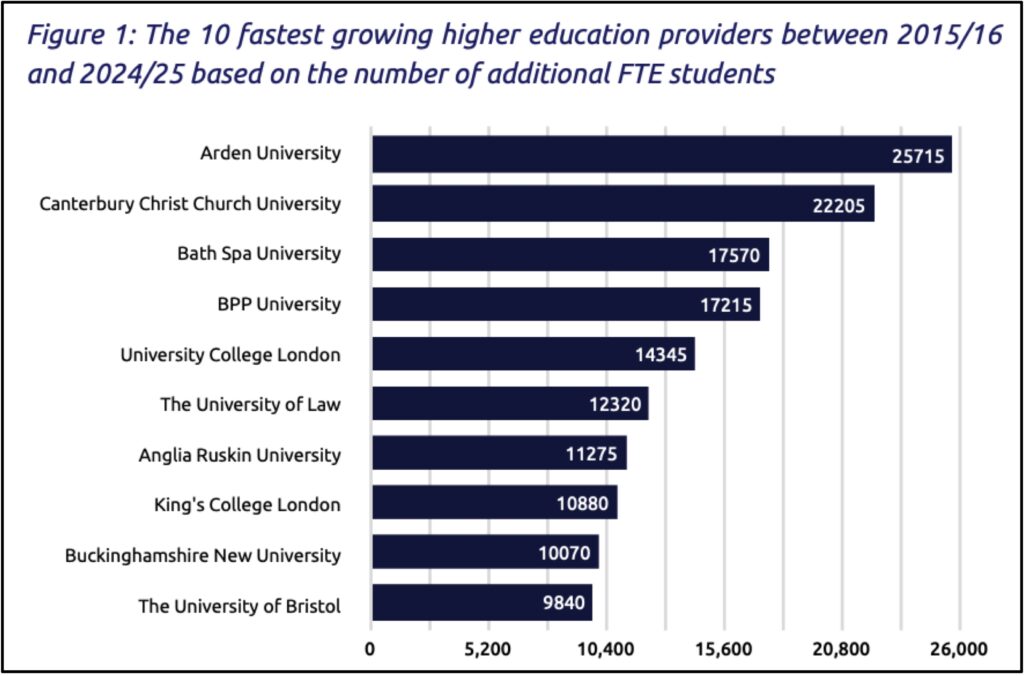

It remains fearsomely hard to get a new provider off the ground and some key policymakers since 2017, such as Theresa May while Conservative Prime Minister and Bridget Phillipson while Secretary of State for Education, have sought to dampen the supply-side measures. Nonetheless, a tiny handful of institutions have grown very rapidly over the past few years – for example, the for-profit franchisee Global Banking Systems (part of the Indian company GEDU) and Arden University (part of the for-profit Global University Systems or GUS) have both experienced very fast expansion and now have tens of thousands of students each despite not being anything like household names.

Looking ahead, Ministers and the Office for Students are focusing more on quality, for example imposing new rules on franchisees. Meanwhile, on the research side, the Government seems keen to concentrate limited research budgets further by nudging some institutions into doing less. It all seems a bit confused, reflecting the reality that the oversight of research is divorced from the oversight of teaching within Whitehall, but the Post-16 White Paper states:

A provider may decide to specialise across multiple disciplines or to focus on one or two where they are strongest. Similarly, a provider may choose to specialise in a specific type of research, which may be more applied or basic curiosity-driven research, or to specialise in teaching. This call to specialise is intended to address the increasing homogeneity in the system.

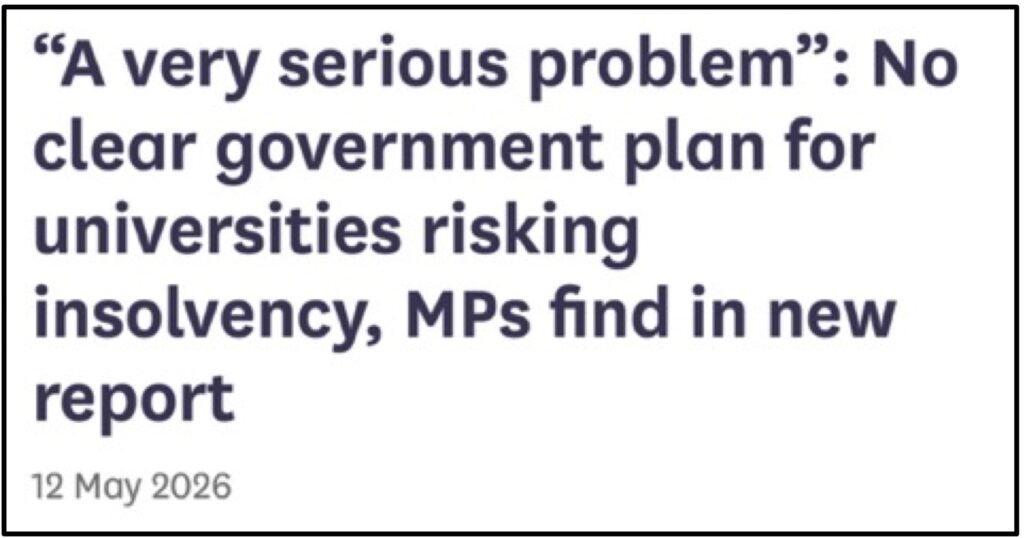

8. Insolvency

Perhaps the single biggest public policy challenge, as identified by a recent paper by the cross-party Education Select Committee, is that no one knows what will happen if and when a university become insolvent – or, rather, some people think they know but they cannot all be correct:

We heard deeply conflicting evidence about what would happen if a university, particularly a Higher Education Corporation or a Royal Charter body, became insolvent. While the Government contends that such institutions could enter liquidation and continue operating, legal specialists and other stakeholders told us liquidation would require immediate cessation of trading.

Just as policymakers who favoured ‘Remain’ did not want to prepare for the possibility of Brexit, fearing that modelling it might bring it about, so policymakers who do not want to see higher education institutions fail have resisted preparing fully for if and when one or more does. Officially, there is no guarantee for any institution – they are ‘autonomous, independent charities’ etc. Yet in practice, it is implausible that even a medium-sized university in a regional town or city would be simply allowed to shut up shop, especially if it were the only such local institution. Too many jobs, too much local prestige and too much past public investment would be in play, and even the most loyal parliamentarian would kick up the biggest stink they could if their own constituency were affected.

Nonetheless, below the line smaller institutions and outposts will close, just as the Southend campus of Essex University is already shutting down and just as some Departments and courses are under threat. Different sources provide different numbers but dozens of higher education institutions have shut in the United States in the past few years in response to fluctuations in demand and demographic change and, as mentioned above, one university in the UK has already fallen over: Dundee. Policymakers say it failed due to weak management and poor governance; others point out the operating environment is worse for universities in Scotland than it is in England. While financial support has been made available to Dundee, this may mean there is less available to support other institutions that find themselves in a similar situation.

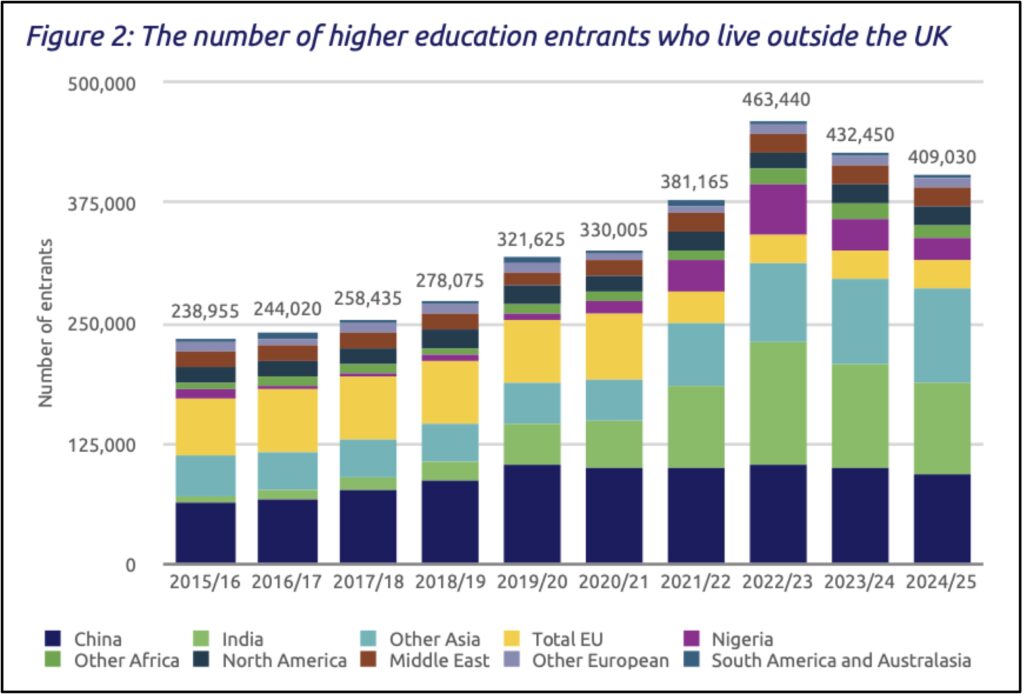

9. International students

The UK higher education sector continues to rest on the shoulders (or the bank balances) of international students and those that fund them, such as their families and home governments. The crackdown on migration after the ‘Boris wave’ has affected students more than most, in part because it is easier to crack down on legal migrants than on those that find other routes to the UK.

There are three legs to the new limits on international students: a ban on dependents for taught postgraduate students (originally introduced by Rishi Sunak); a reduction in the Post-Study Work visa from two years to 18 months; and new tougher Basic Compliance Assessments (BCA) that universities might satisfy to maintain their right to recruit students from abroad.

The third of these puts higher education institutions on the frontline of reducing migration as the new BCA thresholds on things like visa refusal rates force universities to treat applications from some countries more suspiciously than applications from other countries.

In its early days, the Keir Starmer Government spoke a lot about ‘soft power’ but this seemed to slip down the agenda afterwards and the International Education Strategy (January 2026) favours students taking UK qualifications abroad (via ‘transnational’ education) over more students coming to the UK study. Some people expect Andy Burnham’s experience as Mayor of a large conurbation with large successful universities to make him more sympathetic towards international students, as seemed to be the case with Boris Johnson after he became Prime Minister after a stint as Mayor of London. But the pressure on the older political parties from Reform UK continues, which may have an influence on policy.

10. The war against universities

The media love a good negative story about universities and they have been spoilt for choice in recent years, whether the target has been courses with poor graduate outcomes, lecturers pasting trigger warnings on the classics of English literature or the no-platforming of lecturers by protesting students.

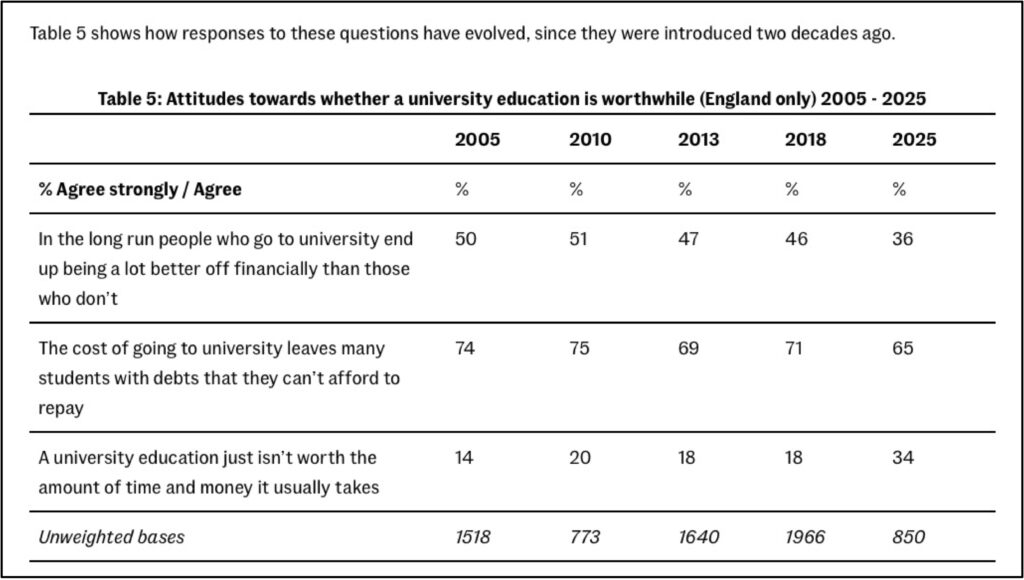

Some of this negativity probably dates back a decade to the time of the Brexit referendum, when universities put themselves squarely on the side of a minority of the electorate and then lived to face the consequences. Either way, the recent British Social Attitudes Survey finding a doubling to 34% in the proportion of people who question whether a degree is ‘worth the amount of time and money it usually takes’. Earlier HEPI work with the UPP Foundation shows a high percentage of the population have never (or not recently) knowingly been on a university campus and also revealed high levels of relative apathy (rather than lots of antipathy) towards universities.

Yet while all the negative commentary has had an impact on perceptions and while some of the complaints may have more than a grain of truth, a majority of people continue to take a more positive view of higher education. One legacy of Sir Keir Starmer’s Government is the official target to increase the proportion of people who participate in higher-level learning of some sort by the age of 25 to two-thirds.

One particularly notable challenge, however, is the striking gap between perceptions of the university sector and the reality: HEPI’s work with the King’s College Policy Institute suggests the median view among the general public is that 40% of graduates regret going to university, while the true figure is just 8%. It seems that none of us has yet found a truly convincing way to rebut such misconceptions without sounding complacent.

Conclusion

In the end, no conceivable future Westminster Government can reasonably expect to deliver its programme, whether that is focused on economic growth, productivity gains, tech-fuelled growth, increased defence and security, improvements in healthcare, transitioning to a green economy or something else entirely, without UK universities.

But no Government will feel compelled to fund the university sector as generously in the future as in the past until we become even smarter at telling our stories, puncturing widespread misconceptions and explaining why the whole country benefits from a diverse, large and successful higher education sector that delivers for students, transforms lives and strengthens the binds that tie society together.

The data and charts come from a range of public sources, including Universities UK, HEPI / Advance HE, the Higher Education Statistics Authority, the British Social Attitudes Survey and the Office for Students. The full sources are available on request.

Comments

Jonathan Alltimes says:

For most of British history, the universities have been peripheral to the ambitions of the British state. It was only when Macmillan commissioned the 1961 Robbins Report did the universities come into view as a new larger lever of government economic policy for industry since then interest in higher education has been in and out of favour, as the promised benefits of higher education have not materialised and the situation is so, as the British state has proved incapable of martialling private investment on a scale which can compete against investment opportunities elsewhere in the world, as examples, the energy and the transport sectors. The slow response of the universities to the so-called industrial revolution followed the technical colleges. Searching around for another later response to British economic decline the ideas of Thomas Balogh about state intervention in industry through science and technology were repeated through Harold Wilson, in which the new research councils could enable higher education to participate. British firms used to working up quickly at scale foreign raw materials into manufactured goods for export, did not like the long lead times for the production of complex goods and once the easy markets and profits had gone, the family owned firms divested.

The account given here is an intellectual tour of the situation. The argument ends by promising the universities are essential for delivering the ambitions of the British state. But the argument does not explain how the situation is likely to cause the British state to fulfill its programmes. What it does not tell is the disconnect between the universities and the private sector. How most jobs do not require graduates and how British firms do not integrate the outputs of government research grants. The reason why the rhetoric of politics has incorporated more about higher education is the British state has failed to the find levers for private sector investment. The error made after the Second World was the failure of the British state to coordinate investment in new industries and the supporting reinvestment in infrastructure, instead it cut taxes to fuel a domestic consumption boom, which it repeated in the 1980s, this time catalyzed with the expansion of credit. Britain is now dominated by the interest of foreign firms, following the Thatcher government policy of foreign direct investment. Part of the answer is the investment profiles of the insurance companies and pension funds, which the state has gone someway towards redirecting. Only insurance companies and pension funds have the time horizons needed for long term investment, as governments and the banks have lost their vision. The other part is reindustrialization and costly technical education and firm-specific training, which mostly the universities do not like, having invested elsewhere.

Reply

Allan Ashworth says:

There are too many universities with overlapping interests in weak subject areas that add little added value in terms of advancement into the world of work.

Reply

Add comment