WEEKEND READING: What’s happening with the UK’s student accommodation?

This blog was kindly authored by Martin Blakey, a commentator and advisor on student living and housing and formerly Chief Executive of the student housing charity Unipol.

2025-26 has been a difficult year for all student accommodation providers and the purpose built student accommodation (PBSA) sector has come under the spotlight as it tries to absorb a number of significant challenges.

This paper follows on from Nick Hillman’s comments made in February 2026 where he asked What is the future for student accommodation? . The fact that such a question is being asked would seem to point to a significant shift in how PBSA serves the student market and how change is taking place – is this just a bad year for PBSA, or are the problems of 2025-26 reflecting more deep-rooted issues that will determine how student accommodation is managed and provided in the future?

The good news

There has been a significant amount of unfavourable publicity surrounding higher education in recent weeks (the loans system, high interest rates and frozen loan repayment thresholds) and the government has been pushing degree apprenticeships and apprenticeships (as part of a skills agenda) with endless newspaper articles asking whether a degree is worth it (almost always written by those with a degree). Despite this, HEPI’s work with the King’s College Policy Institute showed that a mere 8% of graduates regretted their decision to enter higher education, and the OECD’s data showed unemployment was much lower among UK graduates than among non-graduates – irrespective of subject area studied.

In the face of sustained media and political negativity about higher education, undergraduate numbers are still rising (if not by the same proportion to the population). In its January End of Cycle Report for 2025 UCAS reported an additional 12,785 students (+2.3%) with +8,025 (+1.6%) home students and +4,755 (+6.8%) internationals.

Detailed postgraduate figures are not available for 2025-26, but looking at the Office for National Statistics (ONS) main applicants for sponsored study visa figures from October 24 to September 25, there were 434,200 visas issued, up 6.8% on the previous year.

The Higher Education Statistical Agency (HESA) data for 2024-25 also confirms some recovery in the number of international students choosing to study in the UK, after the predictable post-Covid fall in numbers and immigration restrictions coming into force on students with dependents affecting recruitment after January 2024.

The return of the Erasmus+ programme, when it starts, is likely (depending on exactly how it works) to add around 12,000 bed spaces demand. In the last year of its operation in 2018-19 the top three receiving HEI institutions were (in order) Edinburgh, Warwick and Glasgow.

The recent ‘emergency brake’ imposed in March 2026 by the Home Secretary suspending new sponsored student visas for applicants from Afghanistan, Cameroon, Myanmar, and Sudan, based on previous visas issued, is likely to affect only around 0.7% of international students.

The fundamentals of demand for higher education remain sound, so what’s the problem for student accommodation providers?

Demand for accommodation has fallen

After years of warning about how more students are choosing to live at home when they study, the threat of more commuter students can now be clearly demonstrated. The recent data issued by both UCAS (dealing with the 2025 intake) and the HESA data (dealing with the 2024-25 intake) show an unmistakable shift towards full-time students choosing to live at home.

UCAS asks whether students intend to study from home, and within the last 12 months, there has been an increase of 4.4% in students saying that is their intention. So, although the number of students has gone up by 3.7%, demand for accommodation, on UCAS figures, has been almost level at only +0.2%.

The trend, looking from 2016-25, has seen those intending to live at home in their first year increase from 32.9% to 35.2%. Although this does not seem like a large shift, this alone would account for a decline in demand of around 24,000 bed spaces. It should also be recalled that these are figures relating to a single year’s undergraduate entry. In reality, a decline in the demand for undergraduate bed spaces affects three years (assuming the normal undergraduate course span), so that figure of 24,000 (unless there is an upswing in future years for more accommodation) can be multiplied x3 by 2028, with a decline in demand for 72,000 bed spaces. Increasing that concern is that UCAS shows that the preference for studying from home is more enhanced in the mainstream 18 year old cohort, which saw a year-on-year increase of 6.9%.

Looking at the HESA data, the same trend is confirmed. Merging the HESA accommodation categories into two: renting and non-renting (excluding N/A), the total percentage of students renting has shifted from 55.1% to 53.6% from 2023-24 to 2024-25: again, this does not seem like a big shift, but it would account for reduced demand of around 40,000 beds.

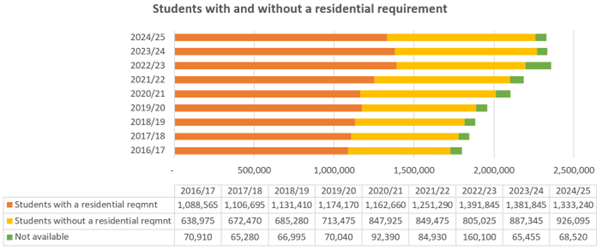

Concentrating on undergraduate entrants with and without a residential requirement 2016-25 the trend away from having a residential requirement is clear.

Of course, the increase in the number of first-year undergraduate students is not taking place uniformly across all HEIs. The pattern of higher-tariff institutions expanding their intake (+7.4% in 2025-26) follows on from the previous couple of years, together with a decline in lower-tariff acceptances (-2%), with middle-tariff universities now seeing some growth (+2.3%).

Nor is the growth of commuter students evenly spread. Generally, post-92 universities have sought to sustain their undergraduate intake by recruiting more students locally, whilst Russell Group universities have recruited the vast majority of their students from those who will need accommodation. Just as examples: Leeds Beckett University has seen students from Yorkshire and Humberside increase from 44.7% of their total undergraduate acceptances in 2016 to 55.0% in 2025, and Nottingham Trent University has seen its students from the East Midlands increase from 33.8% in 2016 to 37.9% in 2025.

These trends have real implications for student accommodation demand: in Nottingham, it can be calculated that demand for first-year undergraduate accommodation has fallen from a Covid peak in 2022-23 of 46,295 beds to 42,290 beds in 2025-26. At the same time supply of PBSA beds in Nottingham has increased by over 7,700 new beds (accounting for 13.8% of all new build beds in the UK over that period).

Also worth noting that (looking at the HESA data up to 2024-25), London is very different from the rest of the UK. In London, there has been no discernible shift towards commuting: a significant proportion of home students have always commuted within London. In London, international students are just over 50% of total student numbers (as opposed to the national average of 24%) but they also form around 54% of demand in the student accommodation market

As the drift to commuting increases nationally, with that not happening in London, it must mean it is happening more in the provinces. If the trend of recruiting more local students continues, this will have important regional connotations for those local economies that rely on ‘importing’ students. It also has implications for universities whose local population is small, restricting growth in that way.

Student maintenance levels

The underlying financial pressure on students’ cost of living and their maintenance loan cannot be overestimated. As the House of Commons Research Briefing in December 2025 summarised:

Inflation was much higher in 2022/23 and 2023/24 than the cash increase in maximum support levels. This led to real cuts in support of 7% in 2022/23 and 4% in 2023/24. The maximum support in 2023/24 was around £1,200 less than in 2021/22 in September 2025 prices (adjusted by CPI inflation). This cut, at 10% over two years, was larger than any real cuts seen in student support going back to the early 1960s.

In January 2023 the IFS said that because the forecasting errors in the previous two years had not been corrected the maximum support amounts will be around £1,500 less in the future.

That briefing also stresses:

The household income level at which a student qualifies for the maximum level of support has remained unchanged in cash terms since 2008 at £25,000.

This means a student with a parent on a minimum wage would no longer be eligible for the maximum level of support. Had this threshold been increased with inflation, NUS estimates it would need to be set at £41,000.

Even then, the maximum maintenance loan (currently worth £10,500 in England) is insufficient to live on, and HEPI’s own research estimated that students needed a little over £20K a year to undertake what might be called a ‘participatory’ level of subsistence.

The major cause of expenditure for students is rent, and in many cases, this eats up a very high proportion of any loan (sometimes more than all of it). Year-on-year, this decline in the ability of many students to afford to live away from home, or to find cheaper accommodation, is eating away at student housing demand, particularly for the more expensive PBSA.

Some of the most expensive PBSA developments (particularly those involving studios) were developed for richer international students. In London, which tends to attract better-off internationals, that market is probably still growing (or its demands have not yet been met), but outside of London, there is an increased cost-consciousness by many international students. Some of that relates to the concentration of Chinese students in fewer locations and their fears that future employment prospects may be more limited than they were, but the type of international student studying in the UK is also undergoing change.

HESA figures show that between 2020-21 and 2024-25:

- the number of Chinese students has remained practically the same at 143,825 and 143,200, whilst Hong Kong is slightly down from 16,660 to 15,755;

- whilst students from India increased from 82,200 to 146,480 and they are now the largest top country sender in the UK;

- Pakistan is a big growth market up from 12,970 to 48,335;

- Nigeria is up from 20,865 to 38,040.

Students from these new growth countries are much more cost-conscious than the pre-Covid students from China, and the affordability of student accommodation is an issue.

Finally, many studios, supposedly developed for better-off international students, exceeded the demand from those students. Whilst there were accommodation shortages, much of this high-cost accommodation was rented by undergraduate students coming through clearing because that is all there was left, and they needed somewhere to live. Now that demand has slackened, this last-minute desperate market no longer exists.

Impact on PBSA suppliers

Occupancy

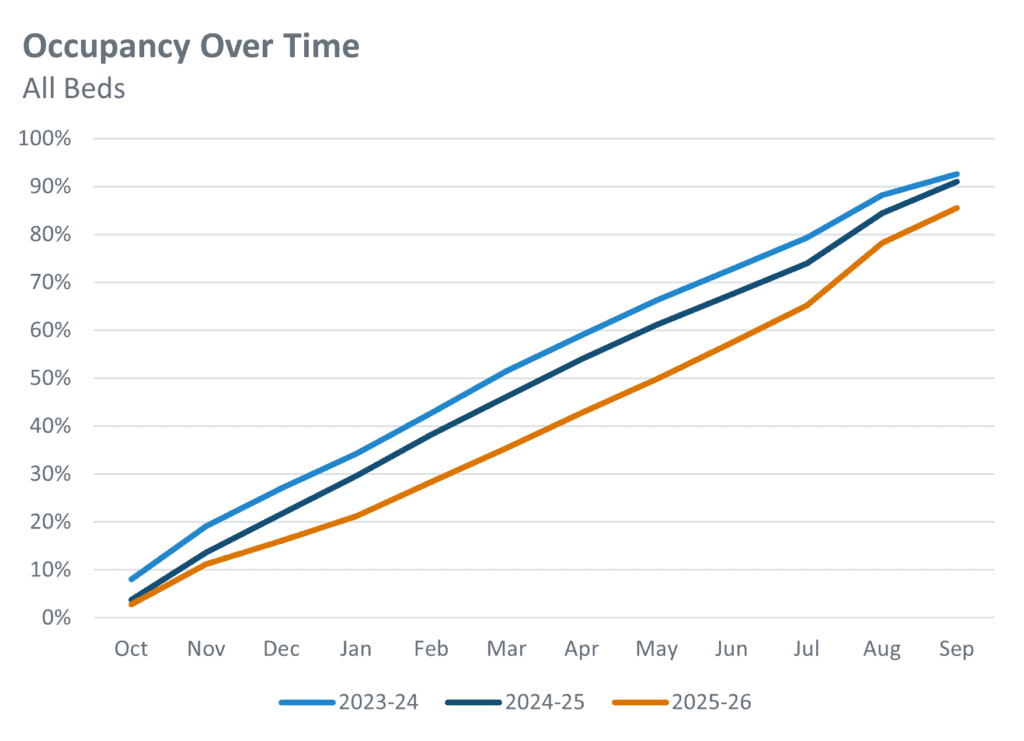

Demand for PBSA has obviously dropped, with very few accommodation shortages now being reported and many surpluses with an increase in empty rooms (known as voids). It is difficult to get accurate data on occupancy, but the StuRents Occupancy Update issued in October 2025 is likely to show fairly accurate occupancy in private sector PBSA for 2025-26. That showed a decline to 85.4% occupancy, down 5.4% year on year. In the pre-Covid era, many PBSA supplies budgeted for between 95%-98% occupancy. The latest figures for lettings for 2026-27 show that by November 2025, lettings were already slightly down on the previous year.

Talking to PBSA suppliers and managers about the 2025-26 letting year, many students were choosing to rent later in the year. Because the previous shortages have mainly abated, students are becoming increasingly aware that they can rent accommodation later in the year (or, in the case of some PBSA whenever they wish). The lack of year-on-year letting comparability results in a ‘loss of nerve’ in the market place with many promotional offers and rent reductions.

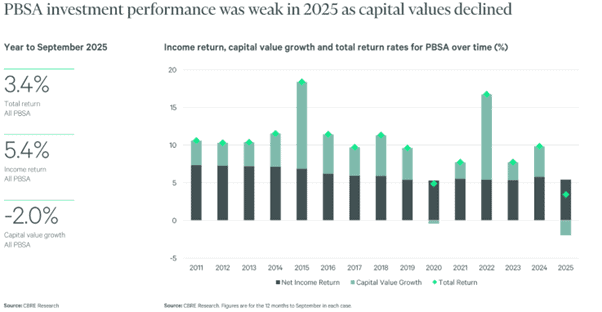

Revenue and capital values

The occupancy figures fail to reflect a falling rent roll, but a report from CBRE shows a fairly dramatic decline in investor returns in PBSA:

As rental income and occupancy falls, so does the capital value of PBSA buildings, lowering anticipated return rates for investors.

2025-26 also saw a significant rise in ‘cashback’ offers, some exceeding £1,000 per let. The idea that giving a student a large amount of cash in one year in exchange for rental obligations they will incur the following year is, at best, irresponsible, and many wonder why suppliers are resistant to lowering rent levels or offering ‘rent free’ periods? The answer to this may lie in accounting mechanisms that can portray cashback as marketing whilst seemingly maintaining an uninterrupted rental revenue stream to maintain capital values. Tricky accountancy aside, large cashback offers are not good news for students and fit badly with those suppliers who claim to act in the best interests of students.

One recent development, as PBSA suppliers increasingly realise the value in the direct letting market of retaining existing tenants (which, according to the Unipol and NUS 2021 Accommodation Costs Survey then accounted for 58% of private sector PBSA beds), is the possible introduction of two-year lets. The student letting market has traditionally let on annual contracts, but some suppliers are now considering the value of offering contracts that are longer with incentives such as a frozen rent level across the years, with perhaps a discount on rent. There was talk of multi-year lettings just before Covid, but it now looks as though this option may now start to come into use.

Other sources of accommodation supply

The reduction in demand for PBSA beds cannot be entirely explained by the greater shift to commuting, and the Build-to-Rent (BTR) sector is beginning to overlap with PBSA and is often not taken into account in industry projections of supply and demand. The British Property Federation (BPF) Who lives in Build-to-Rent? 2025 report showed that students accounted for 30% of renters in Built to Rent Multi-Family Housing (MFH) across the UK. Again, BTR supply and its availability to students will vary throughout the country. In some urban areas, Leeds would be an example; it is likely that student occupancy is up to 40%. It is clear that the BTR sector has become an attractive, high-quality alternative to traditional student housing, with student occupancy growing. To give an idea of scale, there are around 110,000 BTR MFH units now in the rental market (Knight Frank Q2 Market Update 2025).

A third market, Co-living’, is beginning to expand, particularly in London, Birmingham and Manchester. But according to Savills Co-Living Supply February 2025, there are only 9,000 operational units and an additional 5,500 to 13,000 units currently under construction or in the planning pipeline. So their effect on PBSA demand is, at present, negligible.

Evidence on the supply of off-street shared student housing is not collected nationally, but because of planning restrictions, supply will be at best static.

Some analysts have referenced, as an explanation for falling demand, the significant drop in international student recruitment since Covid, but here they frequently rely on recruitment figures that include international students studying with dependents. Of course, PBSA suppliers and shared student HMOs seldom catered for those with families, so it is disingenuous to cite that decline in international demand with a decline in the demand for shared student housing and PBSA.

Other Challenges

The Renters’ Rights Act

The Act will redefine tenure with the near-universal assured shorthold fixed term tenancies ending from May 1 2026, when that aspect of what is wide-ranging legislation comes into force. PBSA who are members of the Government approved ANUK/Unipol Code are largely exempted from the provisions of this Act because they are being granted ‘specified status’ which brings them in line with the university’s own accommodation. This will enable the issuing of common law tenancies, which can impose a fixed term on a contract with a student. There are, however, still risks for PBSA:

- There is a ‘transitional period’ where existing contracts briefly fall under the general assured tenancy status of the Act. Although Government has sought to minimise this risk by allowing wider terms of repossession, this transitional phase will still represent a significant administrative burden on suppliers and may increase tenant confusion as systems change over the start of the next academic year.

- The specified status comes with conditions, in that it only applies to full-time students studying at specified institutions. Some PBSA have argued that they let up to 15% of their rooms to language schools and other private educational establishments who are not specified, and those students will have a right to security of tenure (whether or not they are a student) together with other rights that might mean those additional lettings are no longer viable, driving up void rates further.

- Under the Act, students renting in off-street shared houses will have the freedom to leave their property at any stage, having given two months’ notice, and rent can only be collected 4 weeks in advance. This might make renting from smaller traditional off-street landlords much more cost-effective as tenure lengths may shorten. The flexibility students will have to move between properties at comparatively short notice may also be seen as a big advantage compared with the fixed-term nature of PBSA contracts.

There is real risk here because no one knows how the effects of this major piece of legislation will play out: will PBSA look less attractive because it does not provide tenure flexibility to its tenants, or will off-street landlords letting to students start moving towards catering to non-student lettings, in which case off-street supply could reduce, making PBSA more attractive to returning students?

In any event, as the PBS sector becomes nervous about falling occupancy levels, these legislative changes – which may have real impact – on the sector could not have occurred at a worse time.

Post Grenfell: the Fire Safety Act 2021 and the Building Safety Act 2022

This raft of legislation, triggered by the tragedy at Grenfell Tower in June 2017, is now fully in force. The Fire Safety Act has seen much greater activity by fire authorities, which has particularly affected high-rise student accommodation where detailed risk and condition assessments frequently reveal building defects that now require remedial work.

The Building Safety Act requires a series of ‘Gateway’ approvals for new buildings before they can be occupied and this new system of regulation by a central Building Safety Regulator is still finding its feet. The delays in assessing information and issuing approval by the regulator have led to some lengthy delays in occupying buildings. For existing high-rise buildings, these now have to be registered, and a safety case report has to be accepted in order to continue occupying the building.

Following criticism of the Health and Safety Executive (HSE), which operated the regulatory system, in January 2026 the Government decided to establish a separate and ‘arms-length regulator’ under the auspices of the Ministry of Housing, Communities and Local Government (MHCLG). Although in the longer term, this may address the lack of expertise and the lengthy bottlenecks that occurred within the HSE, in the short term there has been some teething issues leading to further delays.

All of this makes legislative compliance more difficult, time consuming and expensive. It also particularly affects high-rise student PBSA which, as it consists of a significant proportion of high-rise densely occupied housing, is rated high risk and is on the front line as compliance is developed and enforced.

Artificial Intelligence

As systems develop there will be a number of operational efficiencies to be gained from using AI in both managing students and buildings but in the short term, particularly in the area of marketing and promotion, AI is having an unpredictable impact: what happens if a potential resident simply asks “what is the best student accommodation at XXX within YYY price range?” thereby by-passing all traditional marketing methods. Of course, many operators are now looking at how those kinds of questions can be answered in a way that is positive to their services – but, again this uncertainty comes at a time when the letting cycle is itself becoming less predictable.

War in the Middle East

It is early days to assess what effect this will have on the cost of living and the economy generally. But at this early stage of assessment it is worth flagging that interest rates have not followed earlier expectations that they would continue to fall and inflation will increase – neither of which are favourable to the development of PBSA and real estate generally. There will be an effect on international recruitment, although what that effect is remains unknown. Rising energy costs will further increase the operational costs of running PBSA with its “energy inclusive” model.

PBSA development and future investment

It is now generally thought that the previous rapid growth of PBSA screeched to a halt over Covid because of a mixture of higher build cost, higher interest rates and higher operational and regulatory costs. But it is now becoming clear that although the decline in new bed spaces coincided with Covid, a decline from 2018 was already ‘in the pipeline’ and taking place.

The decline in new build PBSA since 2018 has not recovered and what beds are coming on line now are either in London (which can sustain the high price of new accommodation in its growing international market), or reflects buildings that were already ’in the pipeline’ that was contracted at least three or four years ago, with about 29% of bed spaces outside of London being concentrated in Leeds and Nottingham – where there are already a sizeable accommodation surpluses.

The costs associated with PBSA means that some schemes that were ‘in development’ or ‘ready to go’ are being scrapped. The new build pipeline is drying up.

Two publicly announced schemes that were scrapped by Unite were:

- Paddington (a 605 bed scheme that Unite had won on a planning appeal – this incurred a £10m write-off cost.

- Bristol Freestone Island, with 500 beds, has been indefinitely mothballed.

These decisions were made as part of a Unite strategy to ‘accelerate disposals’ (aiming to sell between £300m-£400m of property) and focus on a £100 million share buy-back programme. Unite’s shares have declined by around 43% over the last year (at the time of writing). The impact of Unite’s strategy should not be underestimated on how the sector is viewed by financiers.

Many of those investing in student accommodation are concluding that continued profitability consists of:

- developing high-cost accommodation mainly in London; or

- buying either tired or distressed assets at a much lower price than they could be built for (there are many examples of purchase prices in the provinces being around £60K-£65K a bed space rather than the £110K-£120K of an average new build).

Within the PBSA sector, there is limited expertise in refurbishment, so this type of investment is beginning to generate interest from the hotel sector where refurbishment is inherent in their skill set.

Many previous PBSA investors are now moving into the more traditional house building area, and particularly Build to Rent (BTR) or co-living: the latter having some overlap with student accommodation.

Investors are also turning to other parts of Europe, where their PBSA is more akin to the UK 10 years ago, although, this is not necessarily a guaranteed route of success with The Class Foundation reporting that Dutch higher education institutions in 2025-26 saw a continuing decline in the number of first-year students with Dutch universities seeing falling enrolments every year since 2020, with projections suggesting a near 10% reduction in total students over the next decade.

What is needed in the future?

In the HEPI blog entitled Student Accommodation after 2024 and the Need for Strategic Realignment written in November 2024, three strategic questions were asked:

- How many beds are needed for current and future student use?

- Will students be able to afford them?

- What kind of accommodation should be developed?

The estimates being made then by commercial real estate firms for future student accommodation need now seem, at best, ill-informed and hollow:

- CBRE estimated a shortfall of 620,000 beds by 2029;

- Savills, looked at 20 key markets, concluding that an additional 234,000 beds were needed immediately;

- Cushman and Wakefield estimated that an additional 243,000 beds were needed by 2030.

Many relied on the UCAS projection that there could be up to a million higher education applicants in a single year in 2030 – a projection that, in 2025, is clearly faltering. Coupled with this miscalculation was a denial about the erosive effect of the increased cost of living and declining maintenance support on accommodation demand.

One of the more recent reports, published on 6 January 2026 by Savills (UK Cross Sector Outlook 2026: Living Sectors, Student Accommodation: Becoming more selective ) said:

2025 saw concerns around occupancy levels surface in some markets. Two of the largest (PBSA) providers in the UK reported that reservations were below their level at the same point in previous years in recent trading updates. It is no coincidence that around 150 (HEI) providers failed to meet international recruitment targets for the 2025/26 academic year. As a result, despite 2025 having the strongest third quarter of investment on record, pricing softened by 25 bps through the first nine months of 2025.

Looking forward, investors will need to ensure thoughtful underwriting of locations. That will include a tighter focus on the financial strength and growth potential of individual institutions. It will also mean that selecting the right operating partner will be crucial.

This fairly typical analysis sings the same old song: it is all about international students (despite them being only 24% of full-time students), whereas in the towns and cities with the highest voids, the main cause of those undoubtedly reflects a decline in home student demand.

The reference to strong third-quarter investment could also be misinterpreted: in the main, this is not investment in new developments but consists of investors buying and selling existing stock.

Finally, there is the suggestion of greater ‘selectivity’ for new investment with greater analysis on the financial strength of universities. The implication is that there is some expert pool of knowledge that can be accessed (and paid for, of course) that will show where future investment can make high returns. It is not certain that such an approach holds water any more.

Over the past decade, most real estate advisors advised their clients to major on Russell Group universities and particularly invest in multi-university locations where one of those institutions was in the Russell Group. Investment has followed that advice, often bolstered by the needs of an immediate accommodation shortage. But what has happened?

Some of the highest void rates (empty rooms) are to be found in Coventry (servicing both the University of Coventry and nearby Warwick University), Leeds and Nottingham (where all analysts have flagged over-supply), Unite’s highest void rates (apart from Nottingham) are to be found in Edinburgh, Leicester and Sheffield. All of these have multi-university demand, and all have financially viable institutions.

Some of what looked like risky single institutional investment, such as Lancaster, Lincoln and Loughborough (as examples), are filling their beds in a relatively stable market.

Also of interest is the growth of student numbers and accommodation demand at both the University of Liverpool and Liverpool John Moores University LJMU). Neither university has high numbers of international students, so it is home student demand that has increased, and there has been little increase in the proportion of commuter students over the last few years (despite LJMU’s increasing dependence on the North-West region for recruitment). Could it be that increased student accommodation demand and expanding intakes could have something to do with Liverpool’s attractiveness as a City with a strong local and cultural identity, but where the cost of living is relatively low?

In the HEPI/Unipol Report on Student accommodation costs across 10 cities in the UK 2023-24, the annual average rent at that time for PBSA in Liverpool was one of the lowest of all 10 cities surveyed at £6,467pa, and the average percentage increase in rent since 2021-22 was the lowest at 6.7%. Lower initial rent with the lowest rental rises clearly has some attraction for home students on a tight budget. It would also be remiss not to acknowledge the resources made available by both universities in having good links with private sector providers in the City and really understanding their local accommodation market. At LJMU all their student accommodation is ‘bought in’ and managed by private sector providers but this is within a well-constructed set of underwrite arrangements with regular training and communication events held by the University.

Back in 2024 HEPI Policy Note 52, stressed:

The important point here is that growth in student numbers no longer necessarily equates with the need for additional PBSA student bed spaces as has been the case over the last 20 years: future needs are changing and future accommodation provision cannot, for a whole variety of reasons, be ‘more of the same’.

The Cul-de-sac

To some extent, the PBSA sector is now in such a position. It has continued to develop stock that is both expensive to build (with some commentators calling recent developments ‘an amenity arms race’) and to run. In an attempt to find some economies, new PBSA buildings have been getting larger, with some new buildings coming on line with 1000+ bed spaces – whilst solving some issues on land:build cost these developments have no operational economies of scale and will, in the longer term, cost more to run.

The 2024 HEPI Policy Note 52 stressed that PBSA rents had been rising faster than maintenance support and outlined a possible a new approach to approaching lower rents, including:

- introducing an adjustable energy supplement on rents, encouraging better use of energy;

- organising flats in clusters of 12 to 20 students, around a central kitchen / leisure area;

- smaller pod-sized rooms, perhaps of around 10m2, including en suite;

- good communal spaces for lounge and study areas – especially important when rooms are smaller;

- overnight security only or more co-operation with universities’ own security services;

- buildings of around 300 to 350 student beds, to try and get the best fit on running costs; and

- mixing up room sizes and facilities within one building, with rooms differentially priced.

Unfortunately, there are almost no examples of innovation taking place along these lines – with the possible exception of the partnership between Kexgill Group and the University of Liverpool, where around 350 bed spaces are being developed featuring building conversions and the redevelopment of existing dilapidated units with a strong emphasis on affordability – Liverpool once again showing its strong commitment to affordability.

It is worth noting that those students currently living in BTR have already chosen parts of this lower-cost management model.

So what happens next?

The headwinds against PBSA are clearly strong, and average occupancy levels of 85% will affect both capital values and profitability. What these headwinds signify is that the PBSA model that has seen good levels of returns for investors over the last 20 years (2004-24) is coming to a close, and future accommodation supply is likely to be much more dependent on formal links with the educational institutions that accommodation serves. The days when speculative buildings were constructed, with no links to any educational institution, are (with the possible exception of London) likely to be over.

As student demand has fallen, this gives the student accommodation sector an opportunity to take a development pause and take stock. New development, after the current pipeline has been delivered, is likely to pause for a few years. Pauses have been experienced before and it is worth remembering that student accommodation development has previously taken place in distinct phases with pauses in between:

- The repurposing of (often gifted) buildings by the older universities for student accommodation between 1920-35.

- The building of new student halls towards the end of the 1960’s into the 1970’s, often associated with the new ‘greenfields’ universities that were established but also adding to the stock of the older universities.

- The development of self-catering flats, moving away from catered halls in the 1990’s.

- The PBSA we know today with, developments taking place 2004-18. In the early part of the millennium, this process was often given an additional fillip with the growth in accommodation provision by the competitive, expanding and increasingly confident post-92 sector as they settled into their University status.

In between each of these phases was a distinct pause in activity.

Only in this last phase were universities not at the centre of development, and that is where the sector is likely to head in any next phase.

A rental reset?

There are, of course, other ways that increased affordability for students might be achieved. In classic economic theory, if there is oversupply, with occupancy rates falling and rents that are too expensive, then there could be rental reset: that is, rents could be lowered rather than the last 20 years when they have mostly increased by inflation+.

That reset is probably already taking place, but there are a number of ways this could happened:

- The first is that rents stay at the same level and are not increased for a number of years. StuRents say “In PBSA, rental growth for the 2025-26 cycle was muted, although there were huge variations between schemes.” But in their January 2026 report, they also draw attention to some highly discounted initial offers for returning students renting for 2026-27.

- The second is that investment funds realising that their yield is falling seek to exit the PBSA market and sell some buildings at a discounted price. There are already a significant number of buildings on the market where the bed space price is less than half the cost of new build. New investors are likely to buy these buildings, find some operational economies and offer them at a lower rent.

- The third is that some funds will be losing money and will seek to cut their losses and move on. These ‘fire sale’ properties could also result in rents being lowered.

- Finally, and again, this is already beginning to happen, canny investors are spotting older and tired stock, often in less popular parts of the town that can be purchased at a relatively low bed space cost, refurbished and marketing to students at considerably lower-cost than the high-end city centre products. Students, who might in the past have opted for rooms within a short walk from the university campus, might be willing to have a short travel distance to their institution of study if the price is right.

All of these would constitute a rental reset, and the prediction is that the accumulation of these will result in what could be termed a rental reset taking place over the next 3-4 years.

Part of this reset also requires a resetting of expectations from students themselves, although all the student accommodation officers interviewed this year, have, without exception, made the point that their lowest cost rooms (often the oldest and smallest rooms but pleasant, warm, safe and secure) which used to be hard to let are now their most popular and are let first – so that student adjustment process is already taking place.

What are educational institutions doing?

It is interesting that universities fit into two distinct camps: those that see they ought to be more involved in the provision of accommodation (often via a private partnership); and those that, having disengaged from student accommodation are simply sat on the side-lines watching.

Examples of universities that are increasing their interest in student accommodation would be:

- Exeter (in the first new partnership with UPP for over a decade).

- Sussex (still increasing its stock with Westslope a 2,000 bed development with Balfour Beattie).

- Manchester (with their Fallowfield Campus Development replacing worn-out mid-1960’s accommodation with up to 3,300 new, sustainable student beds).

- The University of Liverpool partnership with Kexgill has already been referenced.

It would be tempting to conclude that investment in student accommodation by universities is all about the richer Russell Group universities, but Manchester Metropolitan University is also investing (demolishing 770-bed Cambridge Halls and replacing them with two new complexes, providing over 2,300 bed spaces, in a partnership with Unite).

There have been downsides to the economies that universities have made effecting demand for student accommodation:

- The University of Kent (now the London and South East University Group – LASEUG) has ditched a £51m plan to build 1,000 bed spaces.

- The University of Brighton is closing its Eastbourne campus, and that will leave some student accommodation providers with problems.

- The University of Essex is closing its Southend-on-Sea campus in August 2026, and its 800 students will transfer to the Colchester campus.

- The University of Nottingham is closing its King’s Meadow and Castle Meadow Campuses.

- In the longer term, the Government’s initiative to encourage campuses abroad may reduce future international student intake.

International online student enrolment (known as transnational education TNE) is also an area of increased activity. This is demonstrated by growth in the number of TNE students at UK institutions overall with HESA figures showing an increase from a total of 489,285 TNE students across all levels and types of provision in 2020–21 to 669,950 in 2024–25.

But, despite all the uncertainties and challenges surrounding university finances, it could be concluded that university-inspired accommodation development is now higher than it was during the rapid expansion of private sector PBSA. Uncertainty in the accommodation market and any rental reset will encourage accommodation developers to work much more closely with universities and there is now a genuine opportunity for a wider range of educational institutions to be able to offer lower-cost accommodation to their students than has been possible over the last few years. Some universities are already involved, and others are sensing that chance.

The Government and policy

In the HEPI contribution Student Accommodation after 2024 and the Need for Strategic Realignment in October 2024 a statement was referenced on 24 October 2024 by the then Education Minister Janet Daby MP saying that the Department for Education was:

working with the Ministry of Housing, Communities and Local Government to promote the importance of a strategic approach to meeting student housing needs to providers and local authorities.

and at that time the HEPI article argued that:

There is a real opportunity here for universities and government to undertake work to ascertain what the real future need for student accommodation will be and then explore how that could be provided and what could be provided. Universities themselves must have a key role in helping to develop new accommodation options, linking future supply to educational objectives and needs: this is not just about housing, it is about what kind of educational opportunities universities should offer students and how this fits into the widening participation agenda.

This fits snugly into the recent comments made by Nick Hillman in February this year (2026), referencing an excellent Times Higher Education piece by Patrick Jack saying

‘n all-round education is one of the UK’s great gifts to the world and it would be idiotic to give it up. After all, people don’t just go to university to get a degree; they go to find themselves, to explore life beyond their hometown and to build new social networks.

and Nick Hillman went on to say:

That argument about the value of the residential student experience has to be made loudly and clearly and repeatedly because, given the perfect storm of rising commuter students, falling real-terms maintenance support and an ever-growing number of university critics, the long-standing arrangements that have worked so well for PBSA (Purpose-Built Student Accommodation) providers for so long cannot be taken for granted anymore.

The value of the residential experience was also stressed in the last Unipol/NUS Accommodation Costs Survey 2021:

Affordability and access are fundamental in maintaining a higher education system that encourages participation from across the full spectrum of backgrounds. While some students will be content to study from home, it would be a seriously retrograde outcome if poorer students were unable to move away from home to study in the way that other students are able to, in keeping with long-established tradition in the UK.

After 16 months of radio silence (and a change of Minister and functions in the Government reshuffle in September 2025) following its inclusion in the Post-16 Education and Skills white paper issued in October 2025, the Government referenced its proposed ‘Statement of Expectations’ with the Education Minister, Josh MacAlister MP, saying

This government recognises that independent students, including care leavers, care experienced students and estranged students, may require additional support to access higher education (HE), including access to student accommodation.

As universities and landlords are autonomous, the department has no remit to intervene in the provision of student residential accommodation. Nevertheless, the forthcoming Statement of Expectations for the HE sector will urge HE providers to plan strategically for the supply of sufficient suitable accommodation for their students and include guidance on how providers can support the needs of vulnerable students.

There is a difference between DfE not having a remit to intervene and taking an interest in residential provision and, as was mentioned earlier, this may be a key time for encouraging that interest in the University sector as they move back into the driving seat on future development and refurbishment.

The Government has given only a broad framework of this statement, but accommodation and support does form one of the eight or so proposed topics. So what might an accommodation statement of expectations cover?

Clearly, there are going to be some obligations stated in respect of ‘vulnerable students’, and that is particularly important relating to students with disabilities, illness or leaving care, but it would be a pity if that was all that it covered. It could suggest, as the Unipol/NUS Student Accommodation Cost Survey recommended back in 2018:

..that, as part of their considerations on value for money, the Office for Students should require those it regulates to have an affordability policy relating to their own and partnered student accommodation, which should contain meaningful commitments to ensure affordability.

Several educational institutions already have these, and King’s College London has The King’s Affordable Accommodation Scheme (KAAS), which provides undergraduate students with capped-price, below-market-rate housing options to support those from challenging financial backgrounds.

The aim of such a policy is to highlight and give encouragement to educational institutions to both take stock of their current residential accommodation costs and consider how a better distribution of lower-cost provision could be achieved.

Comments

Jonathan Alltimes says:

Thank you for the detailed review.

The forecast decline in demand for beds is not a lot when distributed across the higher education landscape, is it?

All the evidence points to a continuing rise in construction, maintenance, and servicing costs, which feed into rents. Competition for renting is likely to intensify and less will be let to students. We are at the end of the journey, as maintenance loans, grants, parents, credit cards, and part-time jobs can not balance the books. People can shamble on for a long time before a collapse.

Individual universities will make their own choices depending on their conditions and constraints, but they may be better off investing their endowments somewhere else other than student accommodation, as the returns are effectively capped by the maintenance loans.

The may be some provision for vulnerable students.

It would good to know the mean mode and range of fixed and variable cost per room for new and for old accommodation for each university (ncluding forecasts), which can then be compared with what students have to spend.

Reply

Add comment