Student Accommodation after 2024 and the Need for Strategic Realignment

By Martin Blakey, the former Chief Executive of the Leeds-based student housing charity Unipol.

On 24 October, Education Minister Janet Daby MP stressed that the Department for Education was:

working with the Ministry of Housing, Communities and Local Government to promote the importance of a strategic approach to meeting student housing needs to providers and local authorities.

So now might be a good time to identify recent trends, cut through some of the developer-led spin that is so prevalent in the student housing world and start considering how future student housing needs may be met.

The questions that any strategic approach needs to answer are simple:

- how many beds are needed for current and future student use?

- will students be able to afford them?

- what kind of accommodation should be developed?

It may also useful to reaffirm why student housing, for many students, is important and necessary, not just to house students near their place of study, but as part of the overall experience of being a student. But at a time of rapid change in higher education, the answers to these questions are, at best, illusive.

Accommodation Demand: the 2024-2025 Intake

Home student intake has been buoyant, despite the gloom in the sector and although UCAS figures show that most of the growth in undergraduate intake has been in higher tariff universities, some post-92 institutions have done better than they expected. Recruitment continued way after clearing and some late recruitment was by direct application, outside of UCAS.

The higher tariff universities have pushed the boat out and taken a lot of home undergraduate students. The last UCAS figures (19 September 2024) showed 137,680 undergraduate admissions. This is a little lower than the peak admissions achieved in the assessed grades year of 2021 at 138,610 and the 2024 intake was much higher than the pre-Covid 2019 acceptance rate at 115,390.

This pattern of intake has an impact on local student housing markets. A senior staff member at Liverpool John Moores University reflected that ‘there have never been more home undergraduate students in this City before‘.

Trying to make sense of local housing demand without detailed institutional data is difficult, but when that data becomes available a pattern may emerge (aside from say the top handful of universities) showing students are opting to study in lower-cost living areas in England. Many of those universities with poorer intakes seem to have been in the more costly South. It is interesting to see several universities begin to market their low cost of living or lower cost accommodation in their recruitment (the University of Huddersfield comes to mind) with some universities making a considerable effort to market their town or city as part of their study offer (as suggested by Ben Sowter in his HEPI blog).

Despite this rise in home intake over the summer of 2024, there were no ‘shock-horror’ accommodation shortages reported this year. Some of this will reflect the decline in demand owing to falling numbers of international students. Again, it is difficult to know how severe this international student downturn is because the most reliable data on this comes from HESA which has only just released detailed institutional data for the 2022-2023 academic year. That data show the peak of international student number expansion and includes the second year of the ‘Covid bulge‘.

The Home Office entry clearance visa applications figures are probably the best available statistics to look at any declining international student trend but there are problems with these: entry acceptances do not necessarily equal ‘bums on seats’ in terms of intake.

Home Office acceptances between January and September were at 350,700, a fall of 16% on 2023 which saw 417,700 acceptances. These figures exclude students who applied for dependent visas which were down 85% (to 17,800 applicants) following immigration rule changes on dependents accompanying taught students that came into force in January 2024. Whilst that reduction in international student numbers may have financial implications for certain universities it is important to recall that very few institutions provide ‘family housing’ for students with dependents (who generally have to obtain their accommodation from within the local housing market) so this decline in students with dependents has had almost no effect on the demand for PBSA or traditional off-street shared student housing.

The main growth area for accommodation will have been at higher tariff universities, which tend to have a lower rate of commuting and a higher rate of students needing accommodation (exceptions being the universities in London and Glasgow) and for them the 2024 pattern of intake will have seen enhanced accommodation demand from home undergraduates. The University of Leeds can be quoted as an example of this, initially planning for significant voids in their own accommodation but as recruitment progressed, they filled their accommodation.

Just a point that undergraduate numbers have increased as PGT internationals have declined, but undergraduate accommodation demand tends to build over a three/four year period (unless intake slackens) so, overall, accommodation demand from undergraduates is likely to continue to increase across 2024-2027 for those institutions with an enhanced first-year undergraduate intake.

The higher growth rate of the Russell Group will have balanced out any contraction in other tariff groups and so undergraduate intake at the larger “red brick” towns has been fairly stable. Whilst most higher tariff universities have filled their own (or nominated) accommodation they have bought in little extra provision in from private providers.

Clearly, there has been less demand for private-sector PBSA and there are significant voids being incurred this year. Partly this is due to fewer international students with the increase in undergraduates being housed through their educational institutions.

But there are other significant shifts in accommodation demand going on.

Cost of Living

Many universities report an increased preference for lower-cost accommodation from both home and international students (at both undergraduate and postgraduate level). There is an assumption that international students are immune from cost of living pressures, particularly from China, but this may no longer be true.

A little reported piece of research by Unipol in 2022-23 (but only written up in 2024) International Student Housing Survey Briefing Paper June 2024 showed that a significant proportion of international PGTs were living in non-PBSA rented housing which fits the theory that the number of students living ‘in the community’ i.e. not in PBSA, is increasing.

Many of the PBSA voids this year can be found in the up-market more expensive rooms and studios so this decline in demand is not just about international student numbers; there is also evidence that students are looking more for mid-price and lower-cost options.

There is also evidence more generally that over the last few years, as the cost of living has outstripped student maintenance loan levels, some students are moving away from PBSA towards either commuting or renting off-street housing. Several universities report that the demand for their first-year accommodation, based on their intake level, was less than they would have expected.

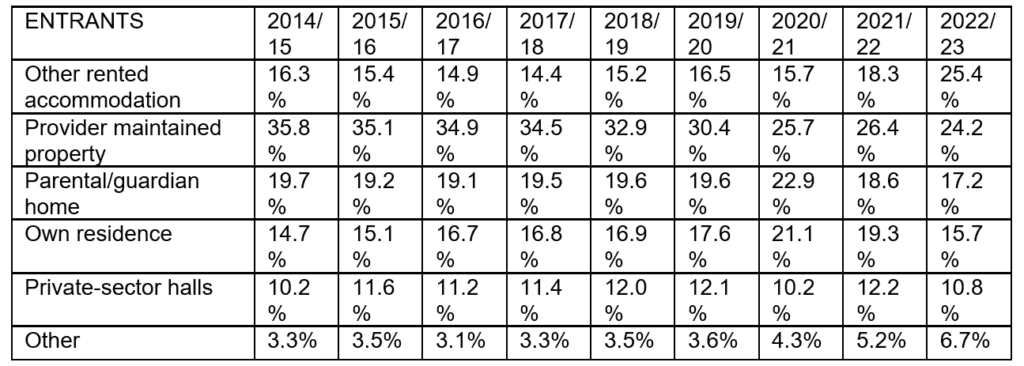

The HESA figures are of interest here. Although some of the data on where students live is of poor quality, it is useful to spot national trends and looking at the data below (analysis provided by Patrick Jack of Times Higher) this shows a clear trend away from ‘provider maintained property’ (down from 30.4% in pre-Covid 2019-2020 to 24.2% in 2022-2023) towards ‘other rented accommodation’ (up from 16.5% to 25.4%). This level of shift is significant.

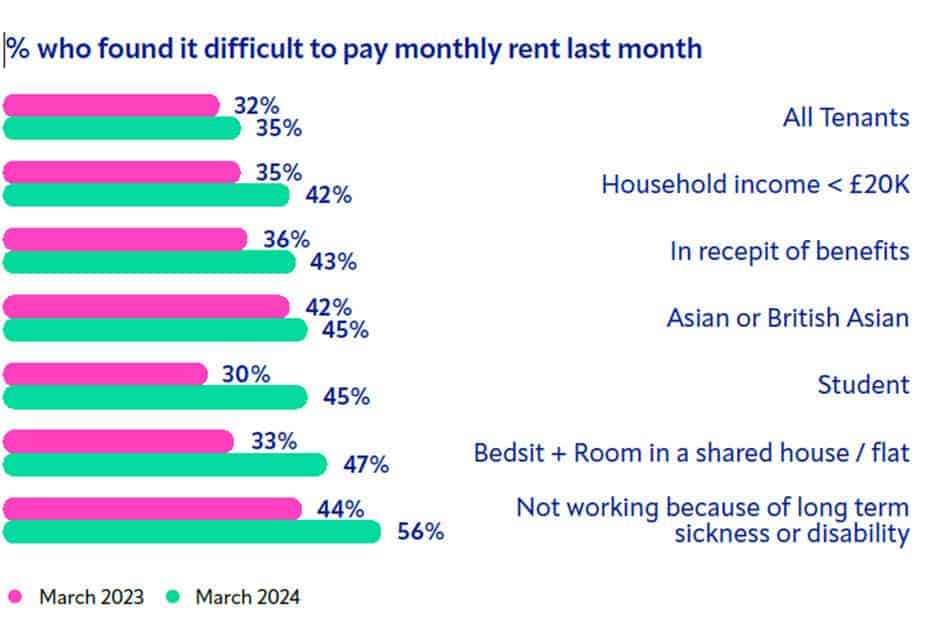

Also of interest is a very recent piece of research undertaken by The TDS Foundation Living in the Private Rented Sector in 2024: The Voice of the Tenant Survey.

This is a regular survey of 2,000 tenants. Only 5% of those tenants are students but the report has an interesting analysis of those having difficulty in meeting rent payments and it can be seen, from the graph below that whilst levels of anxiety for most private sector tenant groups is slowing (as inflation slows) for students that anxiety is rapidly increasing with those who reporting difficulty in paying rent rising from 30% to 45% across the last twelve months.

PBSA Supply

The number of new PBSA additional bed spaces that became available in summer 2024 was very low indeed: only 8,692 new rooms, the lowest level this century. Another 2,500 will come on line during the academic year. These are figures from the Unipol/ANUK private sector Code so they do not include any additional institutional bed spaces, but the view is that any additions (and there are very few this year) have been cancelled out by buildings being demolished or voided for refurbishment/remedial work. Universities are looking at building (for example Newcastle in partnership with Unite, Staffordshire in partnership with Aviva and Sussex in partnership with Balfour Beattie) but all of these are in the future.

The PBSA agents consistently overplay how much is being developed. Cushman and Wakefield report that there are 140,000 additional beds in the pipeline – but, if so, that’s a long pipeline with not much emerging at the other end and they have consistently overestimated the level of year-on-year supply since 2019.

In reality, capital costs are still high (around 5%) and build costs are coming out at £110,000 a bed space (rather than £65,000 as recently as 2018). On that basis, only expensive accommodation (with weekly rents over £200) can be developed or future plans will simply not be viable.

PBSA is generally around 25%-30% more expensive than off-street rents and, although it was thought that the gap may be narrowing, PBSA, as it gets more expensive, is retaining that margin. In July 2024 CBRE analysed the purpose-built student accommodation (PBSA) sector in the UK’s 30 major university towns and London and concluded that rents in the south coast area had increased by ‘as much at 50% since 2021-2022.’

Taking Stock: A New Third Category of Student Occupant

Bringing together these trends:

- many universities have reported an increased preference for lower-cost accommodation from both home and international students;

- evidence is emerging to support the theory that both home and international students are looking more for mid-price and lower-cost PBSA options;

- there is evidence that students are moving away from PBSA towards off-street housing as a cheaper accommodation option with many universities reporting at the start of the academic year that there were significant voids in PBSA but not in off-street properties;

- student anxiety about paying rent continues to increase.

If students are really favouring living in cheaper off-street properties rather than PBSA, how is the off-street market able to absorb these extra students? Since 2010 there have been stringent planning restrictions on converting existing houses into HMOs and that has effectively frozen any additional supply. There is also evidence to suggest that far from increasing, the number of shared student houses has gone down. Almost all shared student housing is also subjected to local authority licensing stipulating the number of occupants as a condition of the license.

How can fewer properties house more students in this regulated market?

Traditionally, student residence has split between those living at home, ‘commuters’ and those renting in their place of study but a third category within the student accommodation market is emerging. These are students who could be termed long commuters: those who live a fair distance away from their place of study but commute and stay for a couple of nights a week, often entering into some ‘sofa surfing arrangement with friends for what is, in term time, a regular weekly stay. This would account for the lower level of take-up of institutional accommodation rented via the University, it would account for a fall in demand for PBSA and it would explain how a full off-street market could (albeit temporarily) absorb more students. Experts in the sector estimate that this third category accounts for between 5%-8% of students, although some put this as high as 10%.

Sarah Jones, a partner at Cushman and Wakefield, hinted at this trend saying:

the shape and nature of the student housing is changing and some of it is hidden from view because we don’t watch the HMO market with the same forensics as we do the PBSA market, but they are so interlinked…..’I think there’s also something about this commuter market. If people are commuting, maybe they just need to be on campus for one or two days a week.

The Cul-de-sac

Any strategic approach by the Government to student accommodation needs to recognise that at the present time, the development of new student accommodation is in a bit of a cul-de-sac:

- off-street housing, because of planning restrictions (Article 4) cannot increase and supply is already declining. This decline will likely be enhanced following the enactment of the Renters Reform Act which increases risk for student landlords. In any event, this sector will be unable to increase supply.

- PBSA is becoming increasingly expensive, particularly the newer buildings. Even with these higher rents, the number of new bed spaces has slowed to a trickle and with high build and interest costs this is unlikely to improve soon.

- the falling value of the maintenance loan is being reflected by students trying to cut their living costs by choosing lower-cost accommodation (where it exists) with some students undertaking long commuting to cut their costs.

There needs to be a sea-change in how new student accommodation is developed and what is provided. The HEPI blog in February 2024 How student accommodation became less affordable and how it could be made more affordable flagged a number of ways that the cost of new student accommodation could be reduced, which included the possibility of:

- organising flats in clusters of 12 to 20 students, around a central kitchen/leisure area

- providing smaller pod-sized rooms, perhaps of around 10m2, including en suite together with the provision of communal spaces for lounge and study areas

- providing only overnight security with more co-operation with universities’ own security services to reduce cost

- constructing buildings of around 300 to 350 student beds, to try and get the best fit on running costs

- introducing an adjustable energy supplement on rents, encouraging better use of energy

In reality, the current PBSA trend is in exactly the opposite direction with planning authorities arguing for larger rooms, higher levels of on-site staff and maintaining all-inclusive rents. These well-intentioned proposals, whilst frequently referencing affordability, achieve exactly the opposite by putting rents up.

Future Accommodation Needs

Student housing shortages have not gone away: the fall in demand from international students and some undergraduates has simply bought time but over the next few years, it is likely that demand will continue to increase. In those areas of existing acute student housing shortage nothing has happened that will provide additional housing capacity.

Any government seeking to promote a strategic approach to student housing needs to try and make an accurate estimate of future student housing needs. At present, the only estimates are those provided by those who sell services to the PBSA sector:

- CBRE estimates a shortfall of 620,000 beds by 2029

- Savills, looking at 20 key markets, concluded an additional 234,000 beds are needed now

- Cushman and Wakefield estimate that an additional 243,000 beds are needed by 2030.

Many rely on the UCAS projection that there could be up to a million higher education applicants in a single year in 2030 – a projection that already looks to be faltering. Bahram Bekhradnia, in his recent HEPI article Student Demand to 2035, highlights that with the size of the young population declining sharply, unless the participation rate for higher education improves, then overall demand for higher education could fall by getting on for 20% between 2030 and 2040. A more recent rejoinder by John Cope suggests that other drivers and economic reality will be much more powerful factors than simple demographics and that future growth will depend more on adult learners, degree apprenticeships, a Lifelong Learning Entitlement and online learning. Whilst these may well be some of the key drivers in future higher education expansion almost none of these students will require specialist student accommodation: they are likely to continue living where they were before they were students.

The important point here is that growth in student numbers no longer necessarily equates with the need for additional PBSA student bed spaces as has been the case over the last 20 years: future needs are changing and future accommodation provision cannot, for a whole variety of reasons, be ‘more of the same’.

Conclusion

So going back to the questions asked earlier:

- how many beds are needed for current and future student use? There is no generally agreed view on this.

- will students be able to afford them? There is already a shift away from higher cost options together with an increase in long commuting

- what kind of accommodation should be developed? At present there is little evidence of any innovation in supplying lower cost accommodation.

There is a real opportunity here for universities and government to undertake work to ascertain what the real future need for student accommodation will be and then explore how that could be provided and what could be provided. Universities themselves must have a key role in helping to develop new accommodation options, linking future supply to educational objectives and needs: this is not just about housing, it is about what kind of educational opportunities universities should offer students and how this fits into the widening participation agenda.

The previous call from UUK and others for universities to become more involved in establishing local student living strategies, talking to their local authority about housing need, has been put on the back-burner as both local authorities and universities grapple with their financial challenges: several early initiatives at various universities have ground to a halt under these day-to-day pressures.

The development model of the past 25 years has probably run its course: it has seen huge improvements in living standards and wellbeing but development has now slowed to a trickle and new PBSA can only be provided at a cost that many cannot now afford. Any new development model must reflect the need for cost and product diversity and must cater to an increasingly diverse and cost-conscious student population.

Back in November 2019, the historian William Whyte presciently identified that:

we urgently need to start a debate about student residence; not because it is necessarily bad, but because we have no clear sense of what it is for. Rediscovering the reasons why British students came to study away from home may allow us to rethink why and how they should do so in the future.

Government and educational institutions need to take an in-depth view about the role, purpose and future scale of student accommodation and that really would fit the bill of delivering a ‘strategic approach to meeting student housing need.’

Comments

David Palfreyman says:

Sounds like a PBSA bubble will burst along with the passing of Peak HE – but probably not before some parts of the PBSA business sector have recklessly committed to bringing on new-build that will be rather short of punters to occupy it!

Reply

David Tymms says:

An interesting paper Martin. I share your view that the domestic and international demographic is changing such that newer, lower cost, design models are needed that increase density to reflect lower income students, which is where HESA data suggests the growth is coming from. However, I am not convinced the direct let PBSA operators will easily break from market norms. I see a period ahead of much lower rent growth and limited new supply.

Reply

Andrew Jamieson says:

No mention of the number of students that have chose to live in BTR schemes, and why? Reduced tenancy lengths? Lower rent than PBSA?

Reply

Hilary Crook says:

The affordability gap between off-street accommodation and PBSA could soon narrow – but not in a way that will benefit students.

I anticipate inflationary pressures in off-street rents from landlords (a) taking advantage of increased demand and/or (b) seeking to off-set perceived risks of the proposed Renters’ Rights legislation. Supply of off-street student housing will contract if students give early notice to quit, their property falls out of step with the traditional academic year, and the landlord looks to other types of tenant. And so the cycle of attrition takes hold in the off-street sector. Increased demand, increased rents, less affordability, more notices to quit, shorter supply, increased demand……

BTR has a role, but some schemes set high-

income acceptance criteria and actively discourage students.

David Tymms’ post succinctly states what is needed and why it is unlikely to appear any time soon.

Unless PBSA is bold enough to break from market norms and provide for lower-income students, the the smartest investment will soon be the sofa-bed.

Reply

Add comment