Why the MoneySavingExpert is wrong

Martin Lewis, the founder of the MoneySavingExpert, is on the warpath. He is furious that the student loan repayment threshold is being fixed at £21,000. This means the terms on which student loans were taken out by today’s students have been retrospectively changed: previously it was said the threshold would increase each year.

- When the freeze was announced last year, Martin Lewis said it was: ‘a disgraceful move and a breach of trust by the Government that betrays a generation of students.

- He then hired lawyers to consider a judicial review and appealed directly to David Cameron for a change of heart.

- He also supported the recent debate in Westminster Hall (an offshoot of Parliament) on the issue – indeed, the Labour MP Wes Streeting was ticked off for noting his presence.

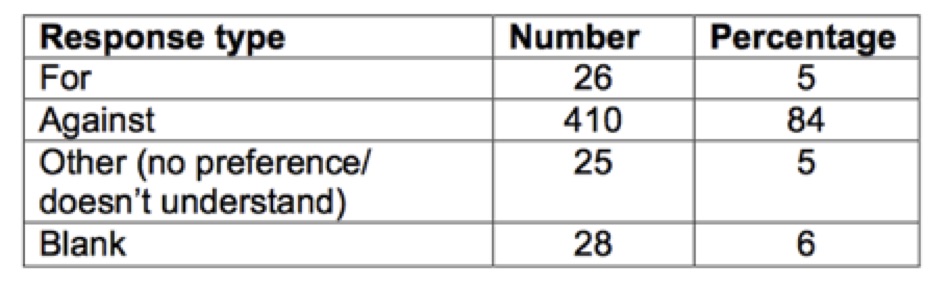

No one likes it when the cost of something goes up, especially when it goes up after agreeing to purchase it. The Government’s consultation on the freeze met strong opposition – there were 410 negative responses and 26 positive ones. It is clearly the job of a website providing financial information to highlight such things, especially when the website is headed up by someone who helped the old Coalition Government publicise how the post-2012 student loans were meant to work. I am not comfortable about the change either, even though I think the abolition of maintenance grants should attract more fire.

Responses to the Government’s consultation on freezing the £21,000 student loan repayment threshold

But there are also strong reasons why Martin Lewis and the other opponents of the change are on less secure ground than has been implied – and not just because the Student Loan Agreement which new students sign allows for such changes.

- First, the MoneySavingExpert says the Government has broken a promise. But the annual increases to the repayment threshold that were promised were the hobbyhorse of the minor party in the Coalition Government in office between 2010 and 2015. Governments cannot bind their successors and that Government left office in May 2015. As the new Government was made up of only the major party from that Coalition, which had never liked the freeze policy, it was always likely to reverse it and was breaking no constitutional niceties in doing so because it was a different entity to the one that had made the commitment.

- Secondly, the increases to the threshold were never more than a verbal commitment: they were not agreed by Parliament even though they had to be to take effect. It was therefore naïve to give them the same sort of weight as things already passed into law – or to assume a new Government that did not like the policy would devote parliamentary time to implementing it. I am no lawyer but starting a legal process against a policy only ever spoken about rather than acted upon seems an odd thing to do (and, indeed, the judicial review went nowhere).

- Thirdly, Martin Lewis has been saying for years that ‘a student loan isn’t really a debt like any other, in fact it acts far more like a tax than a loan.’ Quite right. But taxes change each year. If a student loan is a capped graduate tax, as many people claim, then it is unwise to assume that all its features will be fixed for evermore.

- Fourthly, if (and it is a big if, I admit) the current student loan scheme is deemed to be unaffordable, then it does not make sense to load all the extra costs onto those who have yet to go to university because those who have already entered cannot be affected. Martin Lewis has claimed that the threshold freeze will put people off going to higher education. But if more savings have to be delivered from within the system, they can only come from past, present or future students. Hitting future students even harder than past and present ones could be more likely to affect future demand than sharing the pain.

- Fifthly, we are told the ‘Retrospective changes haven’t happened before’. This is not true (and explains the title of this blog). They have happened before both in the UK and abroad. For example, when the UK repayment threshold rose from £10,000 to £15,000 during the 2000s, it affected all borrowers with income-contingent loans. When New Zealand abolished a real rate of interest on student loans in the mid-2000s, that too affected past and current as well as future borrowers.

Finally, even if you accept that retrospective changes have occurred before, you might well point out that they have tended to help students rather than hamper them. Increasing the repayment threshold (as in the UK) and abolishing a real rate of interest (as in New Zealand) eased the financial position of graduates rather than loading costs on them – the costs were loaded onto taxpayers instead.

But, as we show in a new paper we are publishing today, there are precedents for harsher terms being imposed retrospectively too. In New Zealand the rate of repayment above the threshold rose from 10 per cent of earnings to 12 per cent in 2012. We are not recommending the UK follows but the result, as with the freeze in the repayment terms, was not all bad as it meant debts are now extinguished more quickly, which some evidence suggests many students prefer.

Comments

Claire says:

You might also want to mention that Martin Lewis is trying desperately to cover his own back.

When he was part of the student finance taskforce he went around telling everyone (prospective students & their parents) that the government would pretty much never make any changes. He said it was unlikely and that he’d be able to do something about it if it did happen.

From his point of view it now looks like he was a spokesperson that mis-sold these loans.

What better thing to do than absolve yourself from this blame than to start heavily campaigning against any changes and setting up legal challenges.

Reply

Brian says:

As a student with a pre-2012 loan and a post-2012 loan, I totally agree that Martin Lewis is wrong in saying retrospective changes haven’t happened before. Another example of a retrospective change which certainly didn’t help me in the UK is the 5 year repayment holiday (i.e. break from repayments) that I was promised as a 2008 starter, which had it been implemented, would’ve meant be having the option of not repaying during times when I was a high earner:

On 5th July 2007, the Secretary of State for Innovation, Universities and Skills (DIUS), John Denham, announced that “…we also want to offer graduates more choice about the repayment of their loans. Students starting in 2008 will have that option once they complete their degree. When graduates face significant new out-goings in their lives, such as buying their first home or starting a family, they will have the option of taking a break from their loan repayments. They will be able to take a break of one year, two or more, for up to five years. That will help graduates make flexible choices about their finances at key points in their lives and careers.” https://www.theyworkforyou.com/debates/?id=2007-07-05b.1108.0

Like the threshold uprating, this was a verbal announcement. But I’d say it went further than that as (unlike the threshold uprating) it was included in the SLC documentation: on page 14 of the SLC Guide to Terms and Conditions 2008/09 and 2009/10. http://www.dorsetforyou.com/media/pdf/f/h/2008-09_Student_Loans_-_a_guide_to_terms_and_conditions.pdf

http://webarchive.nationalarchives.gov.uk/20090618153045/http://www.direct.gov.uk/en/EducationAndLearning/UniversityAndHigherEducation/StudentFinance/DG_171624? However, despite this, it was never legislated for.

But as a borrower with both a pre-2012 and post-2012 loan I think freezing the £21,000 threshold was absolutely the right thing to do due to the level of general earnings being lower than was assumed at the start and how my loans now inter-relate (only repayments from above the high £21,000 threshold are used to repay my post-2012 loan which has both higher interest added and a later write-off than my pre-2012 loan, despite repayments being deducted above a current threshold of £17,495. My post-2012 loan has an ever later write-off date than normal post-2012 loans as repayments for this loan didn’t start until 2016 when they otherwise would’ve started in 2014 as I took a one year course).

So freezing the higher threshold helps me as more of my repayments go to paying the loan I’d rather repay. Although freezing the upper interest threshold of £41,000 at the same time means a higher interest rate than if this threshold had been uprated. Wasn’t the RPI to RPI+3% rate taper decided based on the Government’s long-term cost of borrowing being RPI+2.2%? It is no longer RPI+2.2% as the discount rate is now RPI+0.7% so if anything the Government should be looking at lowering the maximum interest rate or raising the £41,000 threshold (if it still wants high earners to pay a rate above Government’s cost of borrowing) so that more lower-earning borrowers pay a rate approximating the Government’s cost of borrowing – even someone earning around £25,500 now pays a rate equal to the Government’s cost of borrowing now that it has been revised down to RPI+0.7%. Lowering the discount rate should result in a reciprocal lowering of the interest rate (at least for lower-earners which could be achieved by raising the upper interest threshold rather than lowering the maximum rate to ensure higher-earners continue to pay the higher rate) and vice-versa.

One of the puzzling things about how a threshold freeze can actually benefit a borrower like me with both pre-2012 and post-2012 loans is how the recommended increase to £21,000 proposed by the Browne Review was implemented by David Willetts and the Coalition Government. Page 35 of the Browne Review recommended “as the threshold has not been increased since 2005, there will be a one-off increase at the start of our new system from £15,000 to £21,000.” https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/422565/bis-10-1208-securing-sustainable-higher-education-browne-report.pdf

But instead of following that recommendation to the letter (i.e. change the £15,000 threshold retrospectively as it had been frozen since 2005, to £21,000), the Government instead implemented a separate threshold of £21,000 to apply from 2016 only for new borrowers.

Indeed in 2010, a Liberal Democrat MP asked: “If raising the repayment threshold is to benefit every single graduate, in the Minister’s [David Willetts’] words, can he confirm that current students—and indeed, current graduates—will see their repayment threshold raised also?” https://hansard.parliament.uk/Commons/2010-11-03/debates/10110358000003/HigherEducationFunding

In reply, David Willetts, as universities minister said: “These are proposals for the future, which come in for 2012. They are not retrospective changes, and for current graduates the existing regime will not be changed. This is only for the future from 2012 onwards. I am grateful for this opportunity to make that clear.”

I’ve never understood how the Browne Review could recommend an increase to £21,000 BECAUSE THE THRESHOLD HADN’T BEEN CHANGED SINCE 2005, yet the Government keeps the threshold which hadn’t been changed since 2005 for existing borrowers and only starts uprating it by inflation in 2012. I know where they got this policy from as right from the start there has been retrospective changes on threshold intentions. This document https://web.archive.org/web/20040117002006/http://www.dfes.gov.uk/hegateway/uploads/final%20RIA%20V8.pdf confirms that it was intended that the original £10,000 threshold (that applied from 1998) would be uprated with earnings. This intention (it was never legislated for) was changed retrospectively as part of the package of reforms that came with variable top-up fees and the 2004 Higher Education Act and it was replaced by an intention to uprate the new £15,000 threshold by inflation from 2010:

37. Raising the threshold from £10,000 to £15,000 will increase the cost of student loans to Government. From April 2010 it is intended that it should increase in line with inflation. However, since the cost of the current loans is assessed on the basis that the threshold will rise in line with earnings growth, there are offsetting savings associated with uprating by inflation instead. The combined effect of the two is expected to be a small net saving in cost to Government over the period during which variable fees will be introduced.

However even the intention to uprate the £15,000 amount from 2010 was changed retrospectively. This should’ve meant (following the Browne Review recommendation) that instead it was increased to £21,000. Starting to uprate a threshold that hadn’t been changed since 2005 in 2012 still seems a very odd decision to me.

Reply

Brian says:

Thought you may be interested in some further digging I’ve been doing on retrospective changes to student loans in my responses here: http://wonkhe.com/blogs/comment-my-word-is-my-bond-freezing-student-loan-repayment-threshold.

One of the things that shocked me was that the repayment holidays policy (although retrospectively changed from 5 years to 2 years in the meantime) was not scrapped by the Labour Government – it was the Coalition on entering office that did not honour it.

The 5 year repayment holidays policy was included in the 2008/09 and 2009/10 SLC guides to terms and conditions as I previously noted. What I hadn’t realised was that the amended policy of a reduction to a 2 year optional repayment holiday for the same 2008 or later starters taking out their first loan and entering repayment in April 2012 or later, was included as a term (page 18) in the Labour version (pre-May 2010) of the 2010/11 SLC guide to terms and conditions:

http://webarchive.nationalarchives.gov.uk/20100315132433/http://www.direct.gov.uk/prod_consum_dg/groups/dg_digitalassets/@dg/@en/@educ/documents/digitalasset/dg_183903.pdf

However in the post-May 2010 version, available here (http://webarchive.nationalarchives.gov.uk/20100519181642/http://www.direct.gov.uk/prod_consum_dg/groups/dg_digitalassets/@dg/@en/@educ/documents/digitalasset/dg_183903.pdf) it had vanished, which meant it was the Coalition that very quietly dropped it.

This was in addition to tinkering with the Labour policy intention of uprating the £15,000 repayment threshold from 2010 (which Labour had postponed for 12 months pending the outcome of the Browne Review as a result of a negative RPI in March 2009) – as the Browne recommendation of an increase to £21,000 was only implemented for new borrowers and the Labour policy of uprating by RPI was not implemented for existing borrowers until April 2012.

Relating it back to the debate on the “retrospective change” to uprating the £21,000 threshold, in a letter to the NUS (http://nussl.ukmsl.net/asset/Blog/23/Willetts.pdf) David Willetts stated that “there have been no changes to the pre-2012 ICR loan repayment terms since 2010, other than for a pre-planned annual increase in the repayment threshold in line with inflation (RPI)”. Clearly, repayment holidays and the planned uprating from 2010 were not yet “terms” as they had not been implemented into the legislation (repayment regulations). This is the same as the £21,000 threshold uprating – which was also not a “term” for post-2012 ICR loans as it was never implemented. So when we’re talking about retrospective changes, we’re (merely) talking about changes to intentions on policy, not changing the terms and conditions – as the HEPI piece above is absolutely correct about.

On the retrospective change to setting interest rates practice in 2009/10 when the RPI went negative but the student loan interest rate (for ICR loans) was frozen at 0%, NUS president Wes Streeting said (http://www.thisismoney.co.uk/money/saving/article-1674618/Government-breaks-student-loans-pledge.html): “in the context of a recession, this is the best deal students and graduates could have expected. NUS will continue to monitor the rate of interest on student loans, and make sure the Government is aware of students’ concerns.”

So both Martin Lewis and Wes Streeting – at the time of previous retrospective changes – did not challenge them and it is therefore totally hypocritical for them now to argue that retrospective changes are ‘disgraceful’; obviously in the case of Martin Lewis it is simply plain wrong to argue that they are unprecedented.

Reply

Brian says:

Thought I would just update to clarify that repayment holidays were actually scrapped by the Labour Government on the quiet in and among Alistair Darling’s final Budget in March 2010, although it was buried deep within a press release and no formal announcement was made regarding the policy being scrapped (despite it appearing in 3 SLC guides to the terms and conditions). This was a political decision to reprioritise student finance budgets as part of the money saved by withdrawing the option of repayment holidays from existing post-2008 starters was used to better the Conservatives’ policy of funding a further 10,000 student places for academic year 2010/11 – Labour announced an additional 20,000 student places in the March 2010 Budget going into the General Election. This is in contrast to the consultation approach pursued by the Conservatives in 2015 when it withdraw the intention of uprating the £21,000 repayment threshold for the time being.

Repayment holidays were withdrawn so quietly that it took a FOI request to confirm for definite when they were scrapped (see below):

https://www.whatdotheyknow.com/request/369590/response/905009/attach/2/DOC051216%2005122016160315.pdf

Reply

Brian says:

On the issue of retrospective changes to repayment thresholds, there are now 2 extremely insightful freedom of information releases on how the policy on this developed with the pre-2012 threshold (notably hardly anyone seemed to acknowledge prior to me raising it that retrospective changes to thresholds and policy intentions occurred with the pre-2012 threshold). There was much misinformation and misunderstanding from the likes of Martin Lewis when the post-2012 threshold was frozen which led to this particular Nick Hillman blog.

In order to further people’s understanding of the retrospective changes which occurred with the pre-2012 threshold I am sharing these FOI releases.

The first shows how the threshold policy developed under the Labour Government. Some people realise that it began life at £10,000 from April 2000. Most people recognise the £15,000 level which it was raised to in April 2005 (not 2006 as stated in the submission below – it seems some people even in Government confuse the year the threshold was raised with the year the new top-up tuition fees came in, which shows the threshold was meant to be reviewed separately to any changes in tuition fee policy). What very few people realise is that it was meant to be raised annually by RPI (at least in the short term, with raising by earnings growth a longer term aim) from April 2010. However the spanner in the works came when RPI was negative (March 2009) at the point it was first meant to increase in April 2010. The following submission shows the 3 options that were considered to the then Minister (David Lammy): (1) decease the threshold by RPI (which happened to be -0.4% in March 2009); (2) freeze it at £15,000 for a further year and uprate by RPI from April 2011; and (3) uprate by earnings growth instead from April 2010. The recommended option was (2) but it was not what happened. The first part happened, as the threshold was frozen at £15,000, but it was not uprated by the March 2010 RPI (4.4%) from April 2011.

https://www.whatdotheyknow.com/request/353572/response/967020/attach/3/Annex%20A%20Repayment%20Threshold%20Redacted%20FOI.pdf

This following freedom of information release neatly dovetails with the above and explains what happened next after the change of Government in 2010. Following much political wrangling in the Coalition Government, an announcement was made in December 2010 by the Secretary of State (Vince Cable) to uprate the threshold in 2012, 2013, 2014 and 2015. The submission to the new Minister (David Willetts) in February 2011 contained this recommendation to implement threshold uprating from April 2012 – presumably this was the earliest that the uprating could now start given that April 2011 was nearing and the above submission shows that practical time sensitive issues with HMRC and the devolved administrations need to be considered. Notably, in the below submission, paragraph 13 identifies that “the inflation increase in the repayment forecast has already been factored into the RAB forecast, so there is no financial impact.”

https://www.whatdotheyknow.com/request/353572/response/939043/attach/5/Gibney%2020936%20Annex%20B.pdf

However, as the first submission shows, the RAB forecast and budget calculations were based on the threshold increasing by 2.8% year-on-year from April 2010, so the fact it was maintained at £15,000 until April 2012 was actually a financial windfall to the Exchequer.

Reply

Brian says:

Also interesting to go with the above and the subsequent post-2012 retrospective changes:

“The coalition says that the threshold for repayment will be set at £21,000, but that is in 2016 prices. In real terms, that is the same as the £15,000 threshold that started in 2006 (sic – it was 2005) and is due for review next year. That is not generous: it is sleight of hand. Lord Browne said the threshold should be uprated every five years in line with earnings. The ready reckoner published by the Department assumes that it will be uprated every five years in line with earnings, but the Minister for Universities and Science, Mr Willetts, says only that there will be periodic uprating. I asked the Secretary of State whether that uprating would be laid down in law, but his letter is silent on that point. Even the dubious claims made about fairness depend on regular uprating in line with earnings, but if it is not in law it means nothing. The House must see draft clauses, not vague promises, before it is asked to vote on the fee cap.” (John Denham, 30 Nov 2010)

https://www.theyworkforyou.com/debates/?id=2010-11-30b.742.0&s=due+for+review+next+year+speaker%3A10167#g746.7

Quite frankly, given the previous developments in 2009-10 with the extended freeze on the then threshold at £15,000 and Browne’s review recommendation (increase £15,000 to £21,000) which was clearly made as a result of the threshold not increasing since 2005 (as the recommendation said so in the Browne review) to bring it back in real terms, if I was in Government in 2010, I would have maintained the threshold at £15,000 until April 2016 (thereby creating offsetting savings as it was budgeted to increase annually from April 2010), amending the regulations prior to the 2015 general election to increase it to £21,000 from April 2016 (i.e. Browne’s “one-off increase”), then periodically reviewing with the aim of increasing it every 5 years to bring it into line with earnings growth over the preceding 5 years or preferably set this periodic uprating down in the regulations rather than leave it to future Governments’ discretion at review. This would also have been fairer on pre-2012 students, not leaving their threshold behind and would have been much less burdensome on employers, HMRC and SLC as a separate second threshold was not necessary. Ironically, we are likely to end up with something close to this after all as the pre-2012 threshold will continue to increase to close in on £21,000 around 2022-23 when the post-2012 threshold will be reviewed. With earnings continuing to fall below forecast, even the expected savings from a 5 year freeze on the post-2012 threshold at £21,000 will be less than budgeted for and so I can only see the “until at least April 2021” threshold freeze been extended to allow for the pre-2012 threshold to catch up to £21,000 and thereafter merging the two thresholds to once again cover all ICR loans with annual RPI uprating. Over the long term, RPI uprating is expected to be less expensive and more sustainable than earnings uprating, as the first submission above noted.

Reply

Brian says:

And… just to link everything up nicely, there’s also this FOI release which is the submission to David Willetts on options for how repayments would be handled for borrowers with both pre-2012 and post-2012 loans (interaction between the two thresholds):

https://www.whatdotheyknow.com/request/230088/response/579884/attach/4/Annex%202%20Submission%20Dual%20loan%20repayments.pdf

As a borrower in precisely this position, to reiterate, I expect (and hope) that the £21,000 level is maintained until the end of this next Parliament (which will now finish in 2022, not 2020) at which point the post-2012 threshold should be abolished as the pre-2012 threshold should by then have reached or be very close to reaching £21,000 in April 2022 or April 2023, given RPI forecasts.

Reply

Dan says:

“…even though I think the abolition of maintenance grants should attract more fire”

As a student who was ineligible for a tuition fee loan (and therefore as a result also would’ve been ineligible for a maintenance grant) due to previous study, the massive increase in the maintenance loan (which is the only aspect I was eligible for) was a lifesaver for me as I wouldn’t have been able to pay my tuition fees without it. So I can’t disagree more with those who say scrapping the maintenance grant was a bad thing!

I don’t know the rationale for why maintenance grant eligibility was conditional on tuition fee loan eligibility whereas maintenance loan eligibility isn’t conditional on tuition fee loan eligibility (you can get a maintenance loan as long as you don’t already hold an ELQ whereas tuition fee loan eligibility is restricted by the formula ‘length of new course + 1 year – years of previous study’ where a student dropped out before completing a previous course. In fact I doubt it was even considered that the policy would particularly benefit such borrowers when it was approved.

But student finance is so fiendishly complex (it’s become too complex really) that certain groups of students benefit from ad hoc changes to the system like this.

Reply

Brian says:

Alas, the freeze on the post-2012 threshold couldn’t be politically sustained and despite for all intents and purposes this retrospective rise in the threshold being meant to help borrowers – in the Prime Minister’s words – “with high levels of debt” (https://www.conservatives.com/sharethefacts/2017/10/theresa-mays-conference-speech), I have a high level of debt but far from putting money back into my pocket, it takes money from me for longer!

And this is very much a retrospective change to my repayment terms (the threshold freeze wasn’t as it merely left the terms unchanged) with the following amendment regulations bringing it about:

http://www.legislation.gov.uk/uksi/2018/284/contents/made

These make grim reading for me as this new policy leaves me in a worse position than I was before. Sadly the people that could see the problems with what the government has done in raising the post-2012 threshold, such as David Willetts, have ended up losing the argument and instead ill-thought through populist policy measures have won out over the evidence (which supported leaving the threshold at £21,000).

WHY THE POLICY OF SUBSTANTIALLY RAISING THE PLAN 2 THRESHOLD (RELATIVE TO THE PLAN 1 THRESHOLD) IS BAD FOR ME

It leaves borrowers like me in a worse position than would have been the case had it remained frozen at £21,000 due to how it alters the division of repayment (set out here http://www.legislation.gov.uk/uksi/2012/1309/regulation/6/made)

which these latest amending regulations do nothing to mitigate.

David Willetts, who introduced the Plan 2 system described Plan 1 repayments as “front-end-loaded” in a recent Treasury Select Committee evidence session:

“Lord Willetts: Not quite. For a student, the repayment threshold and the percentage rate are what matters: the £21,000, now £25,000, and the 9%. One of the reasons for raising the threshold was that I was worried—going back to something else I have written, about fairness between the generations—about people in their 20s and 30s paying back at 9% above £15,000, which was the original Labour government formula. The repayments were front-end‑loaded at a time when I thought people were under maximum pressure.

It was a deliberate feature of the system for repayments not to be front-end‑loaded: to extend further over people’s working lives, so that you were not paying back, in your 20s and 30s, such a high proportion of the amount. That was a deliberate design feature. There are issues about exactly how high the threshold should be, but that was the argument for raising it, compared with the £15,000.”

http://data.parliament.uk/writtenevidence/committeeevidence.svc/evidencedocument/treasury-committee/student-loans/oral/76315.html

Plan 1 borrowers had lower tuition fees so looking at Plan 1 in isolation, the repayments can be seen to be “front-end-loaded” but with greater potential to end sooner than for Plan 2 borrowers. However, this all changes if you then borrow under Plan 2 after also borrowing on Plan 1 as the potential for repayments to end sooner vastly diminishes (due to the massive increase in debt that borrowing under Plan 2 brings with it). So you’ve now got a situation where repayments are both front and back-end loaded which is expressly unfair. For some Plan 1 borrowers (who borrowed prior to 2006) it means paying 9% above the Plan 1 threshold until age 65 and never seeing the benefit of the “progressive” higher Plan 2 threshold despite suffering the same massive debt of Plan 2. This completely disadvantages such borrowers and is surely overly onerous. And borrowers have no choice in the matter: if they hold a Plan 1 loan it is unfair to effectively lock them out of further study by giving them none of the benefits that would ordinarily come with holding a Plan 2 loan. The government is extending loans to second degrees in STEM subjects by relaxing ELQ restrictions so the potential for borrowers who hold Plan 1 loans to borrow under Plan 2 extends to a greater number of graduates. At least such borrowers would know the division of repayment up front and could make decisions on whether to take a Plan 2 loan accordingly.

That cannot be said for me personally: I was grateful for the 2015 decision to hold the Plan 2 threshold at £21,000 as it was allowing me to repay my Plan 2 loan more quickly (so despite repayments being “front-end-loaded” they would have ended sooner). Now, with the division of repayment formula remaining unchanged, the retrospective increase in the Plan 2 threshold relative to the position I was in with it frozen means the same front-end-loaded repayments but more of them going on the Plan 1 loan while the Plan 2 loan continues to accrue interest at the higher rate. So after the Plan 1 period (which ends after 25 years for me as a post-2006 borrower) I then revert to “back-end-loaded” repayments on my Plan 2 loan. It creates one of the most onerous repayment journeys possible. The most frustrating part for me is that the change to the Plan 2 threshold was retrospective – I expected it to be frozen until at least 2021.

Moreover, the government publicy admitted in its 2015 consultation on freezing the Plan 2 threshold at £21,000 that given the slow growth in earnings over the last decade, raising the threshold annually with earnings “is unaffordable in the long term” (https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/447565/BIS-15-445-student-loan-repayment-threshold-consultation.pdf) and that was starting to uprate at £21,000, not £25,000. So for borrowers who hold both Plan 1 and Plan 2 loans who are lucky enough to see any benefit from the higher Plan 2 threshold at all before they retire, given how high it will be now at the start of Plan 2 borrowers’ repayments, there will be greater pressure on future governments to correct this in future by sharply lowering the Plan 2 threshold. And that just so happens to be when those with Plan 1 and Plan 2 loans would start to repay at the Plan 2 threshold (i.e. when it is much lower) so they are at higher risk of being hit both now and later in their repayment period, after their Plan 1 period ends after 25 years. Of course those whose Plan 1 loan doesn’t get cancelled until age 65 may never see the benefit of the higher Plan 2 threshold as the massive debt that Plan 2 loans come with means they never finish repaying either loan. This is because the division of repayment doesn’t allow either loan to be prioritised.

Prioritising more repayments on Plan 1 loans as a result of raising the Plan 2 threshold may well merely be an unintended consequence of the retrospective policy. But I would not be at all surprised if leaving the division of repayment between the types of loan unchanged has got something to do with granting more of the repayments to the purchasers of Plan 1 loans. The government has of course started to sell off these loans. So much for protecting borrowers.

Now that the post-2012 threshold uprating formula is fixed into law, can I assume it’s unlikely to be lowered in future? David Willetts thinks the threshold should still be subject to regular public policy reviews. He said in the same Treasury Committee session I linked to earlier:

“What you are simply trying to do with the RAB charge is estimate, on a set of highly schematic assumptions, how much will be repaid over the next 30 years. It will depend on how things turn out, and it will depend, above all, on public policy decisions, which I very much hope this Committee will influence.”

All this chopping and changing to threshold policy in the last couple of years has left me incredibly frustrated, and with a worse set of terms than what I started with. Yet while people like Martin Lewis celebrate reversing the retrospective change to the terms that wasn’t (the threshold freeze) few realise that borrowers like me have been left to pick up the pieces of the REAL retrospective change.

Reply

Add comment