Why all students should do some Accounting

When, next week, the Office for National Statistics (ONS) rule on the way student loans appear in the national accounts, many people will perform a rue smile.

The Government will be embarrassed because getting student loans off the books was arguably the primary cause of the high fees we have. The way loans are accounted for provided an answer to the question of how to protect institutional income and increase student numbers even in the depths of austerity – but this came at the price of much larger student debts.

People who have always opposed the levels of austerity we have had or who just dislike high fees or who enjoy seeing the political class with egg on their faces will have a field day. Some may hope that, if grants and loans look less different in the national accounts, then grants (teaching grants to institutions and / or maintenance grants to students) might come back in vogue.

But the chickens will come home to roost.

Assuming the ONS put the part of student loans expected never to be repaid on the books, then the policy debate is likely to shift to focusing on how this sum can be reduced.

- One option, currently underway in Australia, is to reduce the repayment threshold.

- Another would be to extend the repayment period, as in the past.

- A third would be to limit student places (just as the number of 18-year olds starts growing again).

- A fourth would be to lend students less money, meaning a less good education or less money to live on.

All four would hit students and / or graduates hard.

I don’t want to live in a world where politicians set their own accounting rules. Then we really would live on the ‘never-never’. Just as the Coalition followed the standard accounting rules back in 2010, so Mininsters should do so now.

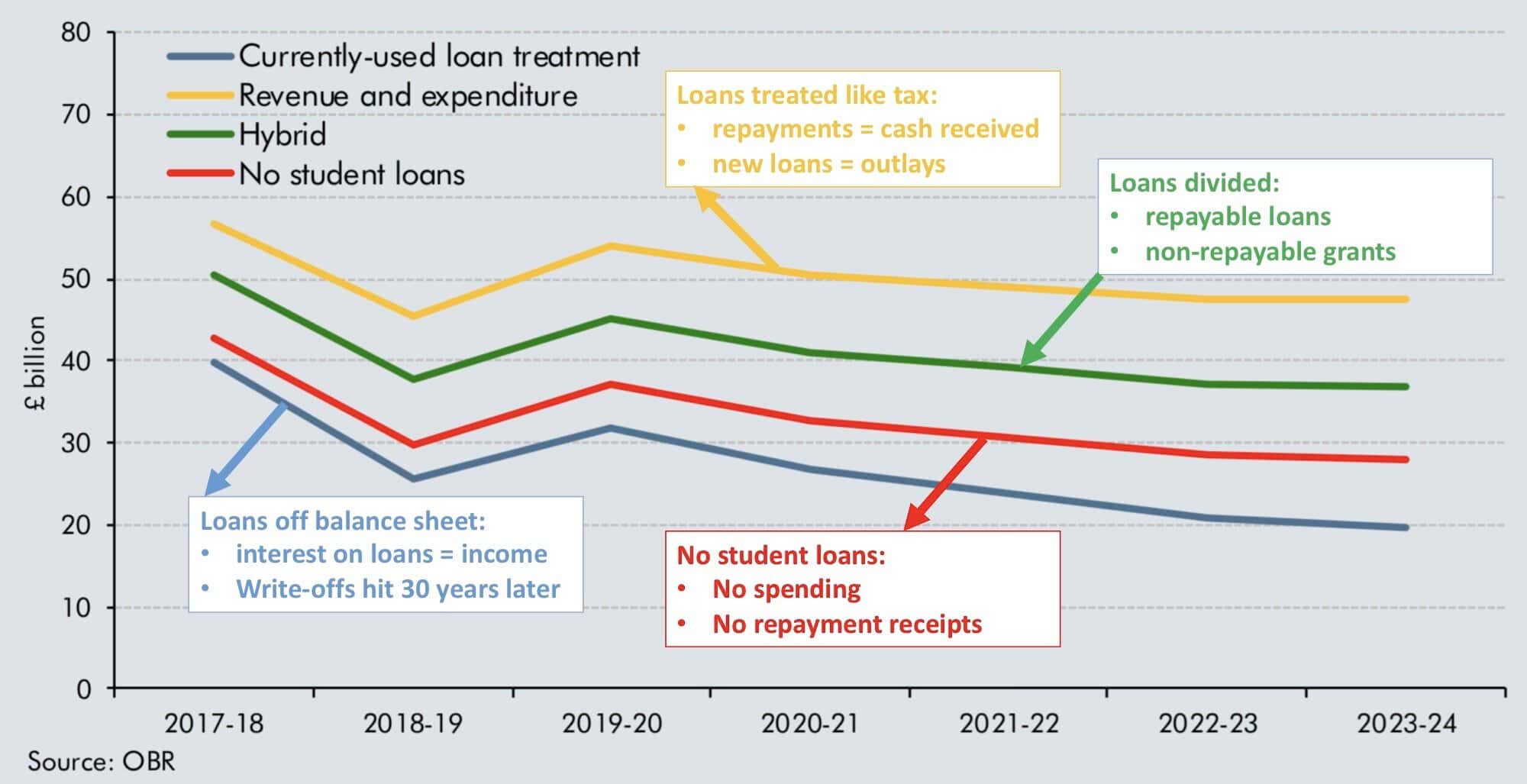

The main options are shown in the chart from the Office for Budget Responsibility (with additions in the form of boxes from HEPI) below. The green line, or something like it, is much the most likely outcome.

But let’s not pretend it’s a painless decision for everyone except the Government. It may be a little embarrassing for policymakers to have to change their numbers, but it is almost certainly students and graduates who will end up paying for it.

The Treasury could try to limit any fallout by claiming any change is merely an accounting change and makes no difference to the real world – they could, for example, ring fence the extra public spending that comes from moving from the blue line to the green line and try to persuade people it doesn’t matter for things like fiscal rules. Yet haven’t we just seen in the recent pensions dispute how technical financial calculations can end up having real world effects?

In short, anyone who thinks the ONS decision is an early Christmas present may find it splits open to reveal some sharp insides.

Comments

Peter says:

Hopefully the Treasury do what you suggest as it has the major advantage of being true – nothing real will change about the affordability of the HE system or about the fiscal sustainability of government spending.

HE will cost exactly the same to the public purse, government borrowing will be exactly the same and the national debt will be exactly the same – it is incorrect to say that student loans are “off balance sheet”.

I share your pessimism though – it’s such a politically totemic measure for the Chancellor and Conservative Party even though it is massively flawed.

One hope is that ONS go for the less radical option of ending the practice of counting hypothetical never-to-be-paid interest of student loan debt as income as at least that’ll stop the flawed deficit measure being targeted having any real-world impact on needlessly cutting HE spending due to misconceptions about what determines fiscal sustainability, with HE spending still outside of the deficit.

Reply

albert wright says:

So far successive Governments have used smoke and mirrors to hide the reality of HE funding.

Whatever the ONS decide it will still be a “Fudge” and not the real truth.

We now must be honest about the cost and benefits to taxpayers.

The loans to students are provided by Government to provide cash income to Universities. This amount must be shown as Government expenditure paid for by tax payers.

I can see the benefit this money provides to the Universities, their staff and suppliers directly and indirectly to the students who have “received” the 45% or so that is spent on their teaching.

The interest that graduates pay seems to go to the Student Loan Company (or to whoever it sells the debt on to) and not the Government. If so it is not income for the Government or a return on Government investment but a windfall to the purchasers of the debt.

The loans that are repaid go to …..? I hope the Government and not the Student Loan Company. If the Government do not receive the money but SLC do, then the only income the Government gets for its massive investment in providing the loans is from the sale of the loans to the SLC which is at a massive discount.

There is thus a huge cash difference for Government between the expenditure on loans and the income received from the sale of those loans.

To help balance the equation we might choose to calculate the estimated additional tax paid by successful graduates who earn above the threshold amount that kicks off the repayment. However, this is hard to calculate accurately.

The ONS decision goes some way to clarify what happens but is little help to the average tax payer seeking to better understand how his taxes are spent.

We are still left with a “stealth tax” reality that moves money from taxpayers to Universities and the speculators who buy the debt.

Reply

Brian says:

I fail to see how lowering the plan 2 repayment threshold hits graduates hard. £25,000 is a very decent salary. At £21,000 graduates were barely noticing the deductions. At £25,725 they think it’s all a bit of a joke and encourages perpetual students: I’m hearing more and more students saying things like “I’m not going to repay what I started with so why don’t I just do as many degrees as possible and milk the system without having to pay a penny back?”

Contrast that to people on plan 1 who are still repaying at the substantially lower £18,330 threshold. If they borrow for further degrees on plan 2 they still have to pay the larger amount and see no benefit from the £25,725 threshold. Perversely if they try to borrow the minimum possible for their later course, that threshold actually penalises them by not allowing them to pay off the plan 2 loan with the longer repayment period (and higher interest). For some graduates, lowering the plan 2 repayment threshold would feel like an early Christmas present.

Reply

Add comment