Why the pandemic is likely to produce a shift in academics’ pension arrangements

The largest private sector pension scheme in the UK …

A couple of years ago, I spent much of the Christmas break in a Reading Room at the British Library. I was investigating the history of the Universities Superannuation Scheme (USS). It was more fun than it sounds.

The report I wrote built on the knowledge I gleaned while working for the pensions industry during the 2000s. It provided some fairly basic reminders about the USS.

For example, it emphasised that the USS is a private sector, not a public sector, pension scheme. Indeed, it is the largest private pension scheme in the UK. This matters, as its status (huge and private) makes it unlikely the Government would ever subsume the scheme, as many people seem to envisage.

(Yes, the Royal Mail Pension Plan was absorbed but the Royal Mail was being prepared for privatisation. With universities, the direction of travel would be in the opposite direction – absorption would pull autonomous universities closer to government, which would be bad for institutions that lost autonomy and bad for government that took on more debt.)

… with the largest deficit …

In my pamphlet, I noted that the USS faced the largest deficit of any pension scheme in the UK. I also pointed out that it is younger than many people suspect, having been established on April Fool’s Day 1975, nearly a decade after the high point for post-war occupational pension scheme membership in 1967. (According to the Office for National Statistics, occupational pension scheme membership doubled between 1953 and 1967 to 12.2 million, after which it fell back to 7.8 million by 2012.)

Despite its relative youthfulness and despite the fact that it has since ballooned to include 340 employers, the USS primarily covers staff (and former staff) at older universities. Staff at newer institutions typically come within the Teachers’ Pension Scheme and there are many other pension arrangements in the higher education sector too (such as the Local Government Pension Scheme, individual universities’ schemes for support staff and schemes for student unions’ sabbatical officers).

The challenges faced by the USS at the time I was working on my paper during Christmas 2018 remain but some have become worse and some have become clearer.

By far the biggest damage [to university finances] will come through its impact on the University Superannuation Scheme, not on things like whether they can keep attracting students

Paul Johnson, ifs

One thing that has become worse is the USS deficit. On one conservative measure, the deficit rose from £5.4 billion to £12.9 billion in the year to March, before the pandemic took full effect (as assets declined by £900 million and liabilities rose by £6.6 billion). Now, according to new analysis by the Institute for Fiscal Studies (IFS), ‘the effect of the pandemic on funded defined-benefit pension schemes sponsored by universities’ is the ‘most important risk to university finances arising from the COVID-19 pandemic.’ In The Times, the Director of the IFS, Paul Johnson, put it even more bluntly: ‘By far the biggest damage [to university finances] will come through its impact on the University Superannuation Scheme, not on things like whether they can keep attracting students.’

… and a high opt-out rate …

One thing that was already an issue back in 2018 but is now discussed more is the comparatively high USS opt-out rate – in recent years, between 15% and 21% of eligible new USS members have chosen not to be in the scheme. In days gone by, occupational pension schemes were deemed so valuable that paternalistic policymakers allowed them to be compulsory. Such a lack of choice did not sit well with the individualism of the 1980s so compulsion was made illegal – and just as the huge additional costs encountered by defined benefit pension schemes began to provide an incentive to drop out.

Given that the pension contribution of each active USS member unlocks a much larger pension contribution from their employer, it seems odd that anyone would refuse to join (especially now that automatic enrolment is the norm for workplace pensions). But having cash in hand now, perhaps in order to cover childcare costs or rent, can be a more urgent priority than having a greater sum gathering up for use in the distant future. (As a new graduate, I opted out of the Teachers’ Pension Scheme. It felt necessary but now it feels like I looked a gift horse in the mouth.)

As a result of such opt outs from the USS, the academic world is not bifurcated – as many people believe – into permanent positions and the precariat. It is trifurcated into permanent positions, permanent posts where the incumbent feels unable to take up all their benefits (like USS membership) and the precariat.

… and among the highest contributions …

In terms of the USS, this is a double whammy as it hits the excluded members of staff and the finances of the scheme. When you combine the USS’s high drop-out rate with the big increase in deferred members (who are no longer paying in but are not yet claiming their pension either), then the level of contributions necessary to fill in the USS deficit remains shocking but does at least become more explicable.

Quite simply, there are fewer active members whose employee and employer contributions are together expected to cover their own benefits and to fill in any deficit than there are deferred members and pensioners. Only 45% of USS members actively contribute to the USS for there are 205,000 active members, 180,000 deferred members and 75,000 retired members.

…. and unusual administrative arrangements.

One of my main sources for the HEPI report was a history of the origins of the USS written by Douglas Logan, the man who did the most to set the scheme up. (His book is more interesting than you might expect too.) The history matters because the problems the USS faces today are largely, though not entirely, a result of how it was established. In short, despite the self-congratulatory tone of Logan’s book, hindsight shows that – in key respects – the establishment of the USS and its early operation are a lesson in how not to set up a new pension scheme.

Some of the decisions should probably have been seen as errors even at the time but others came to look like errors only as the regulation of defined benefit pension schemes changed over time, adding huge costs and reducing important flexibilities that operated as important safety valves for scrupulous employers (but also as ways to cheat people out of pension entitlements – effectively, deferred pay – for less scrupulous employers).

1. Governance

When the USS was founded, the AUT (the forerunner of the UCU) demanded equal representation with the CVCP (the forerunner of UUK) on the USS management committee. Yet as not all USS members were in the AUT, as the employers were set to make much larger contributions than the employees and as the employers accepted the risk of higher future contributions, this was deemed inappropriate.

But the AUT’s lobbying did lead to a Joint Negotiating Committee (JNC), which ‘approves amendments to the rules proposed by the trustee, [and] can itself initiate or consider alterations to the rules’. The JNC had five CVCP (now UUK) and five AUT (now UCU) representatives, plus an independent chair. As a result, the USS ceded significant power to one trades union and what is sometimes described as ‘the vice-chancellors’ club’ as well as to the independent chair, who must resolve the deadlock when the two sides disagree.

Relative to other occupational pension schemes, where employers have more sway, the operation of the USS is messy and conservative. My history of the USS noted that sometimes this had been helpful – I described the positioning of the AUT / UCU on some major issues as ‘prescient’: ‘On issues like protecting the value of pensions through increases after retirement, the union position shifted from being out-of-the-ordinary to mainstream (and even statutory).’

Yet it remains true that, given the burden of contributions lands on employers when their voice is comparatively weak, it has been challenging to drive through the sort of reforms than many people have thought were necessary to bring pension entitlements more in line with those elsewhere in the labour market (including among other employers with charitable status).

2. Contributions

When the USS began, contributions were set at 12% for employers and 6.25% for employees. Over time, the former bounced around more than the latter, as the employers had perhaps unwisely committed to paying for any increases in costs. By 1983, the contribution of employers had shot up by more than half to 18.55% but that of employees was essentially unchanged at 6.35%. However, from 2011, a default ‘cap and share’ rule meant employers would, where necessary, cover only 65% of any future extra increases in cost.

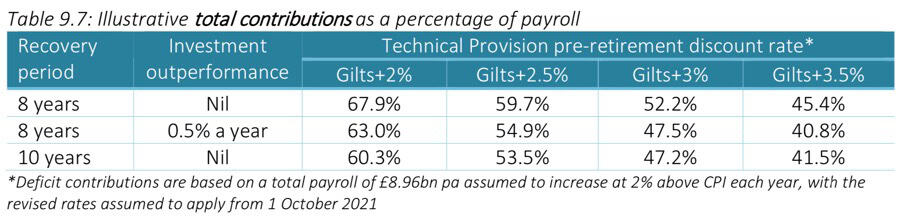

By 2019, employees were paying 8% and employers 18%. Today, the contributions are 21.1% for employers and 9.6% from employees (with further increases planned to 23.7% and 11% respectively). Now, very much higher contribution rates have been mooted, even up to 67.9% of payroll (and the lowest figure is still a staggering 40.8%).

While such contribution levels – which could effectively mean a doubling in employer contributions to over 45% and employee contributions to nearly 23% – are theoretically possible, they are not really plausible if we want to retain a successful higher education sector that seeks a careful balance in the use of its income.

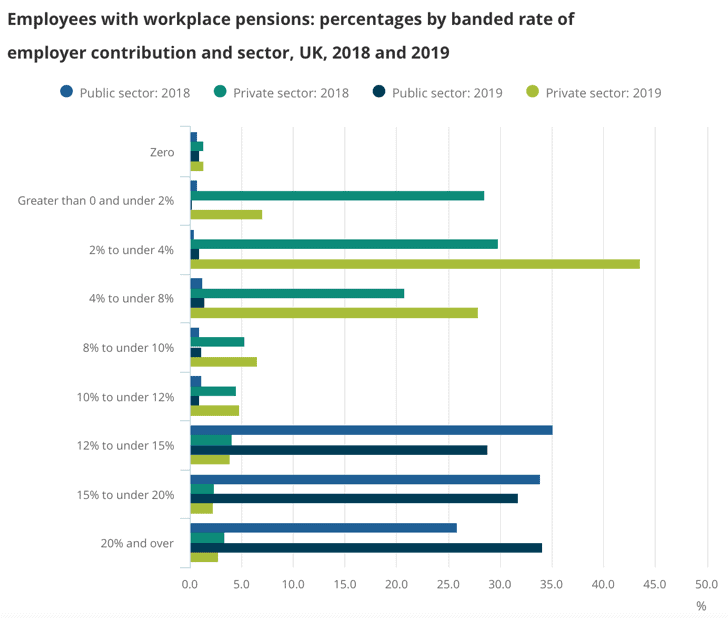

Across the UK, the average employer pension contribution is reported to be 4.5%. University staff count as private sector workers, because universities are independent and autonomous, and over half of private sector staff in a workplace pension receive employer contributions of under 4%. Meanwhile, less than 3% of private sector employees with workplace pensions across the UK enjoy employer contributions at the level offered by the USS, of 20% and over. In part, this reflects the mass closure of defined benefit pension arrangements like the USS, as they tend to have higher contribution levels.

3. Structure

The USS is a last-man-standing scheme, described on one pension website as ‘a multi-employer’ scheme in which ‘the liabilities … pass to the last employer in the scheme where the other employers have ceased to participate or become insolvent.’ This was not inevitable, for it is possible to run a multi-employer scheme in which each employer has their own segregated portion.

A last-man standing scheme does not stop a solvent employer from leaving, as Trinity College, Cambridge, controversially did recently. But this route is not feasible for many: Trinity not only has deep pockets but also had ‘fewer than 20 full-time permanent members of academic staff solely employed by the College in the scheme’. If other employers in a strong financial position were to leave, it would weaken confidence in the USS itself because those that would be left supporting the scheme would be – collectively – less strong than previously. In sort, it would undermine the mutuality that has always underpinned the USS.

The challenge is that the USS was established when there was a deeper sense of the UK having a single higher education system than there is today. Back in 1975, there were far fewer universities, the recent trends towards devolution had not happened and the so-called ‘marketisation’ of higher education, which encourages institutions to compete against one another, was (arguably) still decades away.

Conclusion

Each one of these three factors – the governance, contribution and structural arrangements – can perhaps be defended individually. Together, they have produced a situation where employers are being expected to pay more than they can reasonably afford while employees are paying so much that many potential members feel they must opt out. Some people think bolder investment strategies offer a way out. Even if they do, the Pensions Regulator is sitting in the wings waiting to pounce on behaviour it regards as inappropriately risky.

Overall, the way the USS was established means there is a certain inevitability to today’s problems thanks to the operation of path dependency, where earlier decisions determine later decisions. Some of the heat and anger in recent industrial action over university pensions do not, perhaps, sufficiently reflect that fact. But path dependency is not the same as inevitability and, at some point soon after the pandemic, the USS arrangements will need to be fully reconsidered once more.

In short, despite the controversy and opposition that it will cause, one possible change to the higher education sector caused by COVID-19 could be a reshaping of the higher sector’s pension arrangements, starting at our older institutions that still dominate the USS.

Comments

Indranil Banik says:

I was reading this a few months before starting my first position where I would be automatically enrolled into the Universities Superannuation Scheme. I am grateful to be entering the system at a time when it is clear that the scheme is totally unsustainable, so I am sending my opt out notice many months before starting to ensure I am definitely opted out. In case it helps older academics or anybody interested, I will describe my situation and why I have come to this decision.

I am 29, joining on a fixed term contract. I believe I may be able to continue working in the UK higher education sector beyond the 3 year contract, though that depends on certain factors. In this assumption, for a retirement age of 68, let’s just approximate that I would work for 37.5 years. This means I would get 37.5/75 = 1/2 of my average salary as a pension from 2060. Assuming ten years of withdrawals and an average salary of £50,000, this is £250,000. There is also a lump sum of £75,000. There is likely to be tax on these, so let’s just say that the benefits are surely not over £300,000. Now, the cost is about 10% of my salary, so £5000 for almost 40 years. That amounts to about £200,000. I am quite sure that if I invest the money myself into LISAs and ISAs, I can make £200,000 turn into £300,000 over such a long period. But I would not need to wait so long to make withdrawals – ISAs can be withdrawn any time, and the LISA can be at age 60. So the benefits are already small.

I also have to factor in the inevitability that the rules will change. The benefits are linked to state retirement age. This creates two obvious problems. Firstly, this will reach about 100 by the time I might be able to retire. Secondly, I quite like the work, and so tend not to worry so much about pensions in any case. That is different to not saving – I like saving. But not in that way. In my current role outside the UK where I can’t really become part of a pension scheme, I save about 2/3 of my salary.

The other problem is that part of the benefits are obviously intended for a spouse and dependants to receive in case I fall while contributing to the scheme. Since this scenario cannot arise, it means that part of my contributions would benefit other people but could not benefit me or anybody I care about.

Now, I have no problem with the government saying that they need to help out older people who are poor, and as there are not so many working age people, they need to raise taxes. I am not opposed to the idea of paying higher taxes to help other people out, even if it is for certain kinds of scenarios which cannot apply to me. If the government wants to raise the basic tax rate, reduce the threshold for higher rate taxes, or whatever, I am happy enough. But I am not voluntarily contributing to help this pension scheme. I do not believe either individuals or institutions should enter the USS out of a sense of solidarity towards anybody else. It is an investment plan. If one university really has an obligation to help another one out, then this needs to be part of a larger societal plan, which I doubt universities can sort out on their own.

This brings me to my final issue – loss of control over where the money is invested. I am certainly quite careful to ensure my savings are invested in line with my moral values, and since this is about doing the greatest good for the greatest number, this also usually leads to higher financial returns. So investing into a black box scheme is not too helpful. Especially as I would find it quite difficult to use up my full ISA allowance, and struggle to completely exhaust even the much more limited LISA allowance. So the tax efficiency of a pensions scheme is not that attractive for me.

In short, the high dropout rate for potential new members to the scheme is totally understandable. While individual circumstances can differ, it is clear that entering the USS now is like boarding the Titanic.

Reply

AJ says:

Please proceed with caution.

You make some valid points albeit other factors should be considered which you have overlooked.

We wish you well in the world of academia – but it’s not hopefully in actuarial science!

Reply

LB says:

Indranil, Perhaps your assumption of 10 years of withdrawals is overly pessimistic? Life expectancy for a 29 year old (male) is currently estimated to be 87 and there is a 1-in-4 chance to live to 95 apparently! You could only cover these possibilities by buying an annuity. The current cost for a £25,000 pa income would be more like £500,000 (more if index-linked) which you may have trouble realising with your investment of £200,000

However I would agree that the uncertainties of working on fixed term contracts (which I did from 2003 to 2016) make the decisions more difficult.

Reply

Indranil Banik says:

LB, the cost of the pension scheme is likely to be far higher than £200000 once the rates start going up, so investing an equivalent amount into something else would leave me far more than estimated in the calculation in my comment, especially as the retirement age is guaranteed to go up. Besides, even a £200,000 contribution over 40 years at 9% return (which is typical and about what I get on my savings at the moment) would amount to well over £500,000 at retirement. All this without factoring in the risk of having to leave the UK university sector, which I am not worrying about for the moment. The point is that even with a secure position at a UK university until retirement, opting into the USS is a very bad idea. I agree that of course having an income of £25,000 per year for twenty years would require £500,000 of savings, though actually it’s a bit less once interest is factored in. What I don’t agree is that the best way to build up £500,000 of savings at retirement is through the USS.

Another less serious issue is that even if I did opt in, only about £5000 per year of my savings would go in. I expect expenditures of about £15000 per year and an income after tax of at least £30,000, so I would have to manage a lot of savings efficiently in any case. So it’s not like I can opt into the USS and not have to worry about where all my savings go. But I think it will be difficult for me to save over the ISA allowance, so I think I can get tax-free interest on essentially all my savings without entering a pension scheme.

Incidentally, I noticed some clause in my contract with Saint Andrews about having to leave when I reach the retirement age. This doesn’t really affect me now, and I can sort of understand why it might be in there. I was thinking that for me it would probably be good if the retirement age went up, then I can continue doing what I love for longer.

Reply

Kevin Kingsbury says:

@Indranil … no flies on you.

The USS problem could (should?) be a wake-up call to academics. You generally have high IQ’s and knowledge that arguably should enable smart decisions in the present, for a better future. So why are you in this mess? It appears Western civilisation is precarious, and the group (academics) who the average bloke should be able to rely on to understand and help navigate a path can’t even prepare properly for their own retirement.

I’m not poking fun. I am saying that if you used ten percent of the time current devoted to equality issues (usually Marxist projections) you’d be in a better position.

I hope you get a decent solution to the USS woes – but don’t hold your breath. In the meantime, here are some links which may be part of your individual solution.

Key elements:

Definition of money

Technology (BTC / Blochchain / DeFi)

Counterparty risk

I wish you well.

https://www.youtube.com/watch?v=5OFaZcC0lRU

https://www.youtube.com/watch?v=pkB5ugK0YDY

https://www.youtube.com/watch?v=qL2LfVRl3J0&t=1203s

https://www.youtube.com/watch?v=0tJrla31t8I

https://www.youtube.com/watch?v=k9_bWbrYPKg

https://www.youtube.com/watch?v=QVdZaEJlyDc

Kevin Kingsbury

Reply

Add comment