Reducing the student loan repayment threshold to under £20,000 would save £3.8 billion and lower student loan write-off costs in England from over one-half (54%) to one-third (33%)

Although cuts to any form of education may be regarded as counter-productive in a period of upheaval, it has been widely reported that the Government are looking to make savings from public expenditure on higher education in England at the forthcoming spending review. The Higher Education Policy Institute is therefore publishing some new modelling commissioned from London Economics on various changes to student loans that have been proposed.

The results are being published as No easy answers: English student finance and the spending review (HEPI Policy Note 31). This considers some alternative parameters for English student loans, including: removing real interest rates; an increase in the repayment period from 30 years to 35 years; and reducing the repayment threshold to a little under £20,000. The first of these options would increase the cost to Government while the other two would reduce it.

Nick Hillman, the Director of the Higher Education Policy Institute and the author of the paper, said:

It makes little sense to spend less on education during a time of crisis. There are strong arguments, for example, to spend more on higher education when the labour market is changing so fast, when the number of 18-year olds is growing and when the amount that institutions receive to educate each student has been eroded by inflation.

If, however, policymakers have higher education in their sights for the spending review, then some ways to save money will be more damaging than others. The main options are reducing student places, spending less on each student or recouping more money from graduates by changing the terms of student loans. Cutting places at a time of rising demand is particularly unwise, as is giving institutions less for teaching when their finances are already so squeezed.

Our modelling shows some of the changes to loans that might be made instead. For example, it is possible to reduce the write-off costs by reducing the repayment threshold or extending the repayment period. Such tweaks might not be popular but they could deliver savings if politicians are determined to find them. Reducing the repayment threshold to under £20,000 raises so much it might even enable new initiatives, such as the return of maintenance grants, alongside saving money.

Different changes have different impacts on different groups and we urge policymakers who want to save money by tweaking student loans to use the next few months wisely to ensure the impact is as fair as possible.’

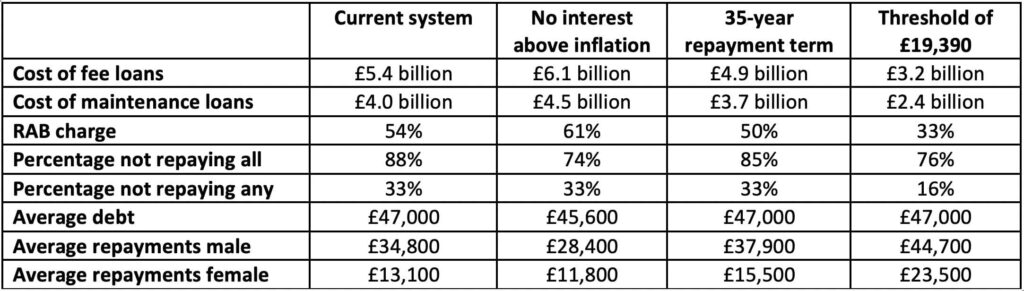

The total cost of English-domiciled undergraduates starting their studies in 2020/21 (plus EU students in England) is set to be around £11 billion: £5.4 billion on tuition fee loan write-offs; £4.0 billion on maintenance loan write-offs; and £1.2 billion on the residual teaching grant (paid by the Office for Students to institutions). The average debt on graduation is expected to be £47,000 and the proportion of loans written-off (the so-called RAB charge) is likely to be 54%. Around 88% of former students are expected not to repay their full loan. Male former students are set to repay around £35,000 on average and female former students around £13,000.

Abolishing the real rate of interest, which is thought by some policymakers to be a particularly unpopular feature of the current system, would have an annual cost of £1.2 billion and increase the RAB charge by seven percentage points to 61%. The impact would be regressive, helping only the best-paid graduates because others do not come close to extinguishing their loan, irrespective of interest, before the 30-year cut off. The repayments of men would fall on average by £6,400 but the repayments of women would fall by £1,300, reflecting the graduate gender pay gap.

Extending the repayment period from 30 years to 35 years would save the government / taxpayers just under £1 billion and reduce the RAB charge by four percentage points to 50%. It would have no impact on graduates with the lowest incomes, who would continue to repay nothing, nor graduates with the highest incomes, who would continue to pay off their full loan before the original 30 years were over. However, it would affect others. The Augar report recommended an even longer 10-year increase in the repayment term, as ‘we believe borrowers should continue to repay their loan for as long as they benefit; we judge this to be 40 years after study has ended.’

Reducing the repayment threshold to match the repayment threshold for pre-2012 student loans (from £26,575 to £19,390) would reduce the cost of one cohort of students by almost £3.8 billion, split by £2.2 billion less on tuition fee loan write offs and £1.6 billion less on maintenance loan write offs. People who studied under the old loan system, before £9,000 fees and loans were introduced, faced a lower repayment threshold in 2020/21 of £19,390. If this repayment threshold were extended to those who currently face the higher threshold, then the loan write-off would fall from 54% to 33%, which is roughly the expected rate when the current system was introduced. It would also reduce the proportion of former students who do not repay their entire loan from around nine-in-ten (88%) to three-quarters (76%) and halve the proportion who never repay a penny (from 33% to 16%). On average, both male and female graduates would repay around £10,000 more. It has been claimed the decision to increase the repayment threshold to its current level was poor value for money. The Augar report said: ‘We question the justification for a system which excludes so much of a borrower’s earnings from any repayment and which helps to reinforce the “no win, no pay” element in student choice.’

Further information, including some additional options for the future, are outlined in more detail in a slide pack produced for HEPI by London Economics that is available to download below or from the London Economics website.

Notes for Editors

1. HEPI was established in 2002 to influence the higher education debate with evidence. We are UK-wide, independent and non-partisan. We are funded by organisations and universities that wish to see a vibrant higher education debate, as well as through our own events.

2. London Economics is one of Europe’s leading specialist policy and economics consultancies and advises clients in the public and private sectors. The Education and Labour Markets team has extensive experience on all aspects of education economics and labour market policy analysis.

Comments

albert wright says:

I think these proposals are a very good way of reducing the cost to taxpayers of educating undergraduates.

Has any research been done to measure possible savings on maintenance loans by, for example having different sizes of loans for those living at home / locally rather than going to a University outside their own region?

The UK is unusual in having a high percentage of students studying far away from their usual residence at 18. Does this lead to a better University experience and if not, could savings be made by offering maintenance grants for “local” undergraduate university tuition only?

Those who wished to go to more distant Universities would have to self finance.

If we are to achieve “levelling up” then local undergraduate education would make a positive contribution quickly as the majority of students find jobs in their home towns or study towns after graduation?

Reply

Nicholas Hillman says:

There is already a lower maintenance package for people who live at home. (Some people think it is too low, given the other challenges commuter students face.) John Denham explored this area a little a few years ago. See https://johndenham.wordpress.com/articles-speeches-and-essays/rsa-lecture-the-cost-of-higher-education/

Reply

Paul Goldberg says:

I am terribly saddened to see this reminder of the levels of debt we are imposing on young people. I wish we could be more like Europe.

Reply

albert wright says:

thank you

Reply

Brian says:

I 100% agree with the policy proposal but the headline figure of “under £20,000” is a bit misleading as by the time the policy would be implemented (probably April 2023) the repayment threshold for pre-2012 loans will have risen to around £21,000 given the elevated RPI over the next year.

The repayment threshold for postgraduate loans is also £21,000 so the policy could be recasted as not only a cost-saving measure on post-2012 loans but also a simplifying one as you could align the repayment threshold for all 3 English ICR plans at the same time to take effect from April 2023.

Reply

Brian says:

There was no announcement of the thresholds to apply from April 2022 in today’s annual updates for post-2012 and postgraduate loans, suggesting change will be implemented as soon as April 2022:

https://www.gov.uk/government/news/student-loans-interest-rates-and-repayment-threshold-announcement–2

Reply

Add comment