Why there should be no surprises about the growing student housing shortage

This blog has been kindly contributed to HEPI by Martin Blakey, the Chief Executive of Unipol. In 2020, Martin co-authored HEPI Student Accommodation: The Facts (HEPI Analytical Paper 2) with Sarah Jones. Unipol publishes the long-running Accommodation Costs Survey with the National Union of Students.

Rising shortages

We are getting used to headlines about student accommodation shortages all over again. This autumn it was the turn of Durham, Manchester, Bristol and Glasgow to be caught in the media’s crosshairs, and they seem somehow surprised about events. Some affected locations have escaped the attentions of the press: Brighton and York also have shortages and others are now getting, at best, very tight supply.[1] These include Bradford (after a decade of a significant surplus), Leeds, Liverpool, London and Newcastle.

But if this all looks like a replay of what happened in the late 1990s, look again. This is not straightforwardly a case of the odd university overshooting its intake target and having to take emergency steps to fulfil their accommodation guarantee. This time round some new things are going on, and they have nothing to do with the long tail of COVID. Hitherto, the impact has been confined to Year 1 students. By contrast, many of the shortages this year are also hitting students entering their second or third years (returning students). In some affected host cities, accommodation shortages are not even connected with increasing student numbers. This blog looks at what is actually going on.

In analysing the causes, I am taking it as read that higher education professionals know accommodation shortages are a major drag on academic achievement. Insecurity about housing can overwhelm the learning experience. For new students, it disrupts the formation of friendship groups and makes transition from home to university more difficult. Having to commute to study takes up valuable time. Living in non-student areas can be isolating and can badly disrupt the ability to do part-time work, which many students now rely on to make ends meet.

Accommodation shortages also mean that many housing suppliers feel they can let anything. Although regulation is always getting tighter, enforcement is often patchy. Nothing raises rents and depresses standards more than a provider’s ability to let anything with a bed in it.

So, what is causing these problems and how are things likely to develop in the coming years?

The causes

Generalising about all university towns and local property markets is a dangerous game, but it is possible to identify some clear factors that are affecting student housing supply. The extent to which these will impact on a single location and university will inevitably vary according to local circumstances.

Just to clarify the terminology:

- ‘PBSA’ is used to mean purpose-built student accommodation, perhaps more colloquially known as ‘student halls’. Shared student rented houses in the community are called ‘off-street houses’.

- ‘Nomination agreements’ are agreements that universities enter into – almost entirely with private sector PBSA providers – to buy in bed spaces in order to ensure they have enough accommodation at the start of the academic year, particularly for first-year, newly arriving undergraduates. Some universities extend the capacity of agreements to accommodate newly arriving international postgraduates, but most do not. Some arrangements are long term, but many are short term – a lot of universities buy in beds each summer.

Even before the effects of the COVID pandemic, many universities were trying to mitigate risk associated with fluctuating intake by shedding longer-term commitments and either buying in beds when there was a known demand (normally late summer) or simply referring students to a source of supply.

During the pandemic, the lack of face-to-face teaching and falling international student numbers meant that many universities ended up refunding rents and paying for empty rooms they no longer needed. This persisted over two academic years and cost institutions a lot of money. The experience has accelerated the growing disinclination of universities to bear risk, which is effectively passed on to private sector PBSA suppliers. In 2017/18, the percentage of PBSA beds underwritten – and thus reserved by institutions for recent arrivals – amounted to 24 per cent of available stock. By 2021, the figure had dropped to 19 per cent.[2] Since 2021 and post-Covid, this trend will have continued apace.

In many towns and cities, with the rapid growth of private sector PBSA, many universities got used to being able to buy in beds at very short notice. In many cases, they had sold their own accommodation and everything they allocated was bought in.

Passing on the risk seems reasonable, but the private sector has sought to mitigate the additional burden by marketing much earlier, letting directly, and letting more of their stock to returning students.[3]

The decline of the off-street shared student house

As a planning instrument available to local authorities, Article 4 Directions remove permitted development rights in converting houses to houses in multiple occupation (HMOs). Their use stops the conversion of family homes to shared houses, and particularly shared student houses. Local authorities can choose to adopt this Direction and almost all councils with student populations did so between 2007-09. The Directions placed a corset on the growth of student on-street housing, as was the intention. Over the last 10-to-15 years, increased demand for student housing has had to be met by the growing PBSA sector – or students have had to commute.

The number of off-street student houses has also fallen, as landlords have either sold back into owner-occupation or moved markets to rent to professionals. This shift is difficult to quantify, but individual records on council tax exemption show a consistent decline in on-street student accommodation, as housing pressures on younger professionals have increased. This switch to other housing groups is particularly marked where there is also a strong professional graduate letting market, such as in Bristol, York, Brighton and Manchester.

Over the past couple of years, the drift from student to professional renting has become more pronounced. Landlords housing students have not had a good three years. In 2020/21 and 2021/22, students pressured them for COVID rent refunds. Where these were not forthcoming, bad debt and bad feeling increased. This year, 2022/23, providers renting on a bills-included basis had set their rents before energy costs soared and the higher-than-planned energy is costing them dear (around £3,000 for a five-bed shared house).

Many landlords have been looking with new eyes at the rented sector for professionals. Compared to the student sector, the business case is compelling: no Covid refunds, lower management effort and more consistent demand. Added to this, rents are rising, as the country consistently undershoots its new-build housing targets (last year by 40 per cent), and as access to purchasing houses is constrained by higher house prices and higher interest rates.

In Leeds, Unipol is in a position to monitor these shifts. Despite stasis in PBSA bed spaces and university intakes in 2022/23, the number of on-street bed spaces available to let in September 2022 dramatically reduced from the previous year. In September 2021, there were 1,166 bed spaces available. As of 22 September 2022, this had fallen to just 205 rooms. The student houses that had left the market were mainly smaller, three- or four-bed houses, easily switched into professional lets.

The Renters Reform proposals

Under the Government’s Renters Reform proposals, tenants will be able to maintain security of tenure and also give two months’ notice. That students living in on-street housing will be not be treated any differently as tenants has unsettled the market: because student landlords will find it hard to predict when a property (and rooms in a shared house) will become available to let, there will be major disruption to the annual cycle. Already, these proposals are speeding up the exodus from the student market and into professional renting.

The Scottish Government recently commissioned the UK Collaborative Centre for Housing Evidence to review student accommodation. Its conclusions on the effect of recent tenure and renting reforms in Scotland are clear:

When the new private tenancy arrangements for Scotland were legislated for in 2016, this reflected a decade of regulatory change in Scotland culminating in open-ended tenancies, finite and reduced means of repossession by landlords and a 28-day cooling-off period for tenants at the start of tenancies. It was agreed that students living in university halls or PBSA would be exempt from this legislation, and that they would continue to be housed under a common law contract with the provider rather than a legal tenancy.

However, the majority of students living away from home would continue to be in the HMO private rented sector and would be covered by the new tenancy arrangements, thus creating a division in rights and law depending on what form of accommodation students choose (or can access).

It is now widely accepted across the sector that as a result of the new tenancy and the experience of Covid-19, private landlords who hitherto had been content to let to students are now moving away from that market and looking for more long-term tenants with less chance of void periods. The evidence from Glasgow and Edinburgh appears to suggest that this is shrinking the available supply for student HMOs and putting upward pressure on rents. (August 2022)

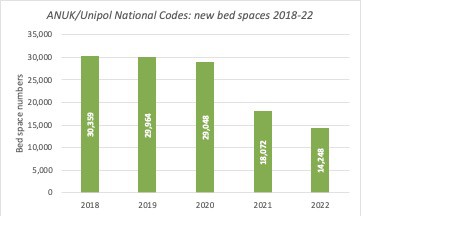

PBSA growth is slowing

Just as students are becoming heavily reliant on PBSA bed spaces, growth in stock is dramatically slowing. Figures from the National Codes show PBSA bed spaces increasing at around 30,000 a year across 2018-20. Earlier figures are not available, but they were probably at that rate throughout most of the 2010s. Last year, new bed spaces fell to 18,072. This was initially attributed to delays caused by Covid operating difficulties, but the persistence of low figures of new-build PBSA into 2022 (14,248) gives the lie to that theory.

At the same time that the supply of new PBSA provision is falling, more and more existing bed spaces are being withdrawn for upgrading or remedial works. For 2022/23, it is estimated that 10,000 beds left the sector for this reason.

The number of new beds coming into commission in 2023 is likely to be similar to 2022. Beyond that, two strong headwinds will come into play:

- increases in construction costs; and

- rising gilt rates amid major recent uncertainties in the financial markets – the level of gilt rates affects the funding that underpins the development of new PBSA beds.

Taken together, these factors will further slow development until at least 2025.

Students with dependants

The latest shortage is probably the most unreported of all – accommodation suitable for students with families. Many universities are now ramping up recruitment of international students from India and Nigeria, mainly onto taught postgraduate programmes. A significant minority of these students are bringing their families with them. PBSA has never catered for this small but growing segment, and most universities have very limited accommodation for families, if any. These students have to take their chances in the general rented housing market in their locality. In some university towns, finding suitable accommodation is difficult for student families. This is an entirely unquantified problem, but most accommodation offices report serious difficulties in this area.

Conclusion

So, lots of reasons why accommodation shortages are occurring:

- universities reducing their underwrite agreements and securing fewer rooms for their first-year students. When they do react to the possibility of an overshoot in intake, institutions are leaving it too late in the year to buy in provision, because beds have already been let;

- the response of private sector PBSA operators to bearing greater risk is to market to returning students;

- the decline in the number of on-street student bed spaces, as landlords move out of the student sector. This means that more returning students are living in PBSA;

- the renters’ tenure reform proposals causing instability in the supply of on-street student housing; and

- the slowdown in the growth of PBSA at exactly the time when returning student demand is on the up.

These factors are likely to grow in significance to make accommodation shortages more common in the future. The last time this happened was the late 1990s and the solutions that institutions used then – camp beds in sports halls and doubling up rooms with bunk beds – would no longer be acceptable today, either to students or for health and safety reasons.

How might accommodation suppliers and universities react to these circumstances. Housing supply is always a long-term challenge, but here are some immediate suggestions:

- Universities need to look at housing demand and supply for all their students across all levels and years of study, because, in an accommodation shortage, those last in the queue suffer most. That will be first-years first and foremost, but, as supply contracts and demand increases, so shortages affecting returning students become more apparent;

- Institutions need to be more honest about their accommodation offer. From the student’s point of view, offering an accommodation guarantee and then placing them in housing many miles away does not count as the university honouring its pledge; and

- Institutions could start developing a more strategic approach for housing all their students. The pioneering Student Living Strategyput together by Nottingham City Council and both local universities is a good example of an informed and joined-up approach.

Greg Hurst’s Could universities do more to end homelessness?, published by HEPI this July, makes several recommendations that encourage fact-finding, raising awareness and coalition-working to approach housing strategically. This publication also references a prescient personal story from Professor Mary Stuart (a former Vice-Chancellor of the University of Lincoln) about her difficulties finding a home as a student family. It concludes:

Homelessness sits at one end of a spectrum of housing issues and universities should explore their own position, not only in providing research on the issue or ensuring that relevant degree programmes teach their students about homelessness, but also by understanding the situation of their own student population.

One thing is for certain: as accommodation shortages become more apparent, statements like ’the university is engaged in a dialogue with the city’s letting agents and is in touch with the local authority’ or ‘we must have enough student accommodation – just look at all those cranes’ will ring increasingly hollow. An informed proactive approach is essential.

Finally, with proper information and knowledge, no one should be ‘surprised’ by a shortage: they are a predictable outcome of trends in supply and demand. Would it help if Unipol published a list of next year’s ‘surprises’ now?

[1] A case study of Bristol was included in the Unipol/NUS Accommodation Costs Survey 2021, p.36.

[2] Ibid, Figure 46, p.62. The survey also shows the shifting balance of ownership of purpose-built accommodation since 2012/13. In 2012/13, institutions laid claim to 60.9 per cent of total provision, and the private sector to 39.1 per cent. By contrast, in 2021/22, universities accounted for less than a quarter (23.6 per cent), and the private sector for more than three quarters (76.4 per cent) – see Figure 42, p.60.

[3] The private PBSA sector has grown quickly over the last few years, in contrast to university-provided bed spaces. This shift was mapped in the 2021 Unipol / NUS Accommodation Cost Survey: private sector direct lets were found to have increased by 114 per cent and covered 58 per cent of all beds let.

Comments

Peter Mills says:

A very helpful analysis that hopefully reduces the excuses for inertia on this issue. I would add that there is a regional and sub-regional dimension also. The short term consequence will be more commuter students.

Affluent students living in major conurbations and/or with decent transport links will have the greatest scope and choice. If you live in peripheral areas of the north, the rural east, Wales or the south-west, then opportunities are most definitely closed off.

As Martin flags, universities need to be much more careful in thinking through the housing consequences of particular decisions. For example, quite a few universities operate a first come, first served policy for first year accommodation, that comes into play prior to UCAS deadlines for students to decide their firm and insurance choice – U of Nottingham and U of York being examples.

Not only does this ride roughshod over the spirit (if not the substance) of UCAS principles concerning the avoidance of undue pressure over choice selection, it aggravates an already difficult situation.

Reply

Steve says:

“the number of on-street bed spaces available to let in September 2022 dramatically reduced from the previous year. In September 2021, there were 1,166 bed spaces available. As of 22 September 2022, this had fallen to just 205 rooms.”

This number falls well short of the total number of “on-street” beds in Leeds and presumably, only represents a small sample of the market, which may not be representative of the whole city?

It would be great to see the data underpinning the assumption that HMOs are in decline. National data covering Class N council tax exemptions show a long-term increase up from 212k properties in 2019 to 230k in 2022.

Reply

albert wright says:

The solution, as ever, lies in contrarian thinking and seeking the answer in the paradox to the question asked.

New Universities should be built in places that do not yet have a university.

The “Student housing shortage” is the result of too many students, applying for too many places in already overcrowded student cities.

It is made worse in the UK, by the desire of too many UK students seeking to go to a university outside their local place of residence, plus the high number of foreign students applying to the same, crowded Universities.

We must encourage fewer students to seek an undergraduate degree and instead look at local Apprenticeships at levels 4 and 5 at a local FE College as their way forward in life.

Of students still going to University, more should study locally and stay local after graduation.

For those who need to go to specific institutions outside their locality, specialist accommodation needs to be built.

Reply

Add comment