Why policymakers should look at student loan systems in other countries before making changes

I had the pleasure at speaking at one of the excellent webinars organised by the Centre for Global Higher Education (CGHE) the other day. Ostensibly, the event was an opportunity both to talk about HEPI’s recent publication with London Economics on the options for changing student loan features and to hear a response to this work from Professor Lorraine Dearden of UCL, who has thought deeply and written widely about the student finance system.

The webinar attracted a stellar international audience, including the Australian architect of the first national system of income-contingent student loans for tuition (Bruce Chapman), so the discussion following my presentation may be of interest to many readers of the HEPI blog. If so, it can be watched back on the CGHE YouTube page.

Regular readers of HEPI output will know our paper outlined the reasons for not cutting education spending in a crisis before noting that this might nonetheless occur and then modelling three options for the future English student loans system:

- removing the real interest rate;

- extending the repayment term from 30 to 35 years; and

- reducing the repayment threshold for post-2012 students to the rate faced by earlier cohorts (which is a little under £20,000).

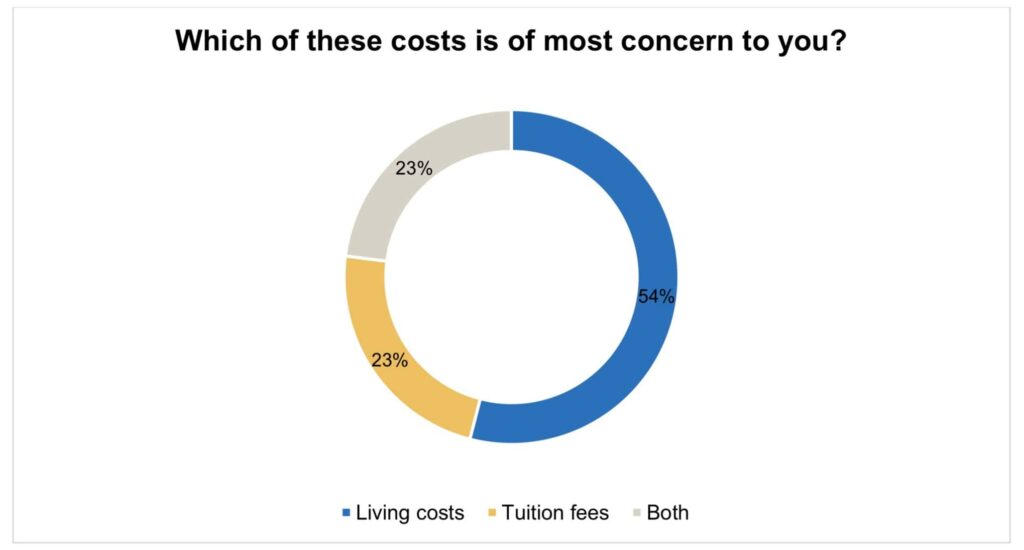

The first option actually increases the cost to government but was included in our modelling. because Chris Skidmore and other former Ministers for Universities are keen on the idea. The second saves taxpayers £1 billion. The last of the three ideas saves so much (£3.8 billion) that we recommended that, if Ministers were tempted to make the change, they should consider using some of the savings to reintroduce maintenance grants. That could tackle the situation whereby the poorest students emerge with the biggest debts and, depending on the implementation details, it could help ease the cost-of-living challenge. In the new HEPI / Advance HE Student Academic Experience Survey 2021, we find more concern about living costs than tuition fees.

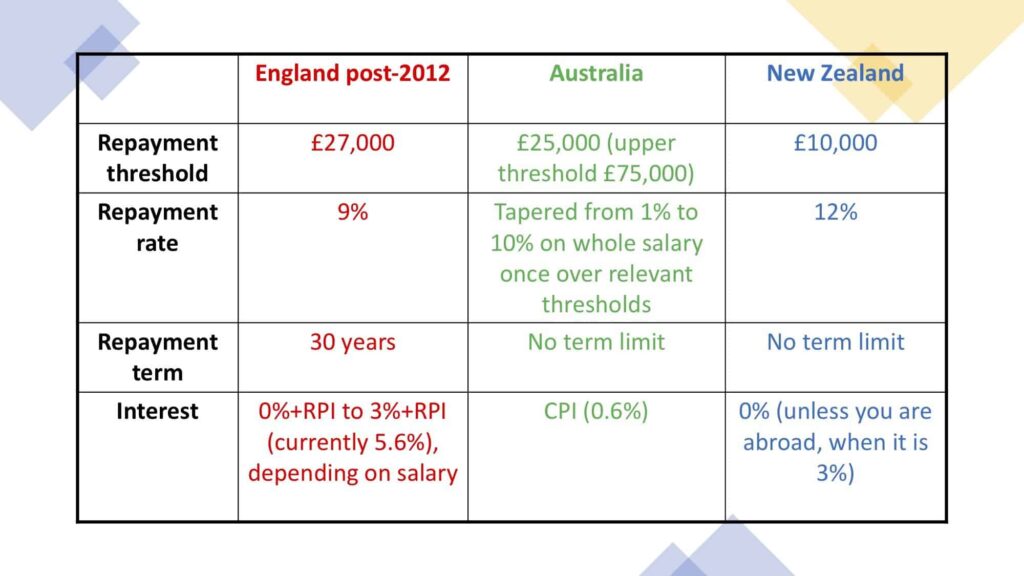

One thing we did not consider in our paper on tweaking student loans but which I did flag at the CGHE event is that policymakers could be wise to look around the world at other student loan systems before making any tweaks. I produced a very top-level chart looking at just four features of the English / Welsh, Australian and New Zealand student loan systems:

- the repayment threshold;

- the repayment rate;

- the repayment term; and

- the interest applied.

(We did not look specifically at the rules for Scotland and Northern Ireland, which are somewhat different to the rules in England and Wales – see here. And, as Wales has kept maintenance grants, the calculation that some of the savings from tweaking loans could be reinvested in maintenance support may look different in Cardiff compared to Westminster.)

NB Between July and September 2021, the maximum interest rate in England / Wales is 5.3% rather than the 5.6% shown because interest is ‘capped in line with the prevailing market rate for comparable unsecured personal loans’.

Various things stand out from the comparison with other countries.

- In some ways, the parameters of the loans in the English / Welsh system are notable for their generosity. For example, in New Zealand and Australia unpaid loans are not wiped out after a fixed period of time – just on death – but they are wiped out after 30 years in England and Wales.

- Moreover, the repayment threshold itself is marginally higher on this side of the world than in Australia (which is a reversal of the past) and it is much higher than in New Zealand. This means graduates can earn more before they need to start contributing some of their income towards paying down their loan.

- In addition, the repayment rate in England and Wales (9%) is lower than the rate in New Zealand (12%, which was increased from 10% back in 2013). The English rate is higher for most of those repaying than the Australian one (as repayment rates there vary from 1% to 10%, depending on income). However, once the repayment threshold is passed, in Australia repayments are based on someone’s entire income, not just the amount above the repayment threshold. So someone on the equivalent of £26,000 in Australia will pay 1% of their income (£260) in repayments but a comparable person in England / Wales would pay nothing back (and someone in New Zealand would pay back a hefty sum not far short of £2,000).

- In other ways, the English / Welsh system looks quite tough – for example, the high real rate of interest during study and, for higher earners, after graduation means debts grow more quickly and are paid off more slowly than they would be with a lower rate of interest or no real rate of interest above inflation. In New Zealand, if the graduate remains in New Zealand, debts are not even linked to the rising cost of living so ‘inflation becomes your best mate’ by eating away at your debt.

- In terms of complexity, the tapered interest rate applied to graduates in England and Wales is rather more complicated than elsewhere (and seemingly quite poorly understood); on the other hand, the flat repayment rate of 9% is much simpler than the tapered repayment rate in Australia.

Comparison with other systems is useful: it shows that other parameters are potentially palatable to voters, that tweaks to loans need not change the way the system works overall and that no one system is perfect. Comparisons can only ever be taken so far, of course, and it is notable that the average student loan debt taken out in Australia and New Zealand is typically much lower than here, which might put the repayment rules in a different light.

Comparison with other systems is useful: it shows that other parameters are potentially palatable to voters, that tweaks to loans need not change the way the system works overall and that no one system is perfect.

Moreover, there are other options beyond those already in place in other countries, like the one Lorraine Dearden argued for at the CGHE event of a substantial (20%) upfront ‘loan charge’ or the much higher interest rate pushed by a group of students’ unions.

Comments

Add comment