High inflation could devastate universities and leave students feeling overwhelmed by debt

This blog was kindly contributed by Mark Corver, Founder of DataHE. You can find Mark on Twitter @markcorver.

Inflation in the UK has been at modest levels for thirty years. And it remains so. For May 2021 the Retail Prices Index (RPI) statistic recorded a 12-month price change of 3.3 per cent. An entirely unremarkable reading for the past few decades. But it was triple the rate from November 2020, and a good number of leading indicators for inflation are strong both in the UK and around the world. Both CPI and RPI inflation data for June will be released later today. The month to month values are often variable, but the recent trend has been upwards.

Some reason that these stirrings, with the context of exceptional levels of pandemic-response money creation by central banks, suggest much higher inflation could lie ahead. Others are more sanguine, expecting a short burst of inflation that quickly settles back to the previous modest level before it has time to establish itself in higher wages. In truth, no one knows. But if inflation were to return it could interact with the way most UK university students are now funded and turn a slow burning resource problem for university leaders into a funding crisis alarmingly quickly.

Inflation is difficult to measure. The RPI has some statistical drawbacks meaning it is no longer seen as a good choice. I use it here though as it has a long time-series and because its main weakness – being biased upwards – seems to trouble the government less when it comes to setting the interest rate on student loans.

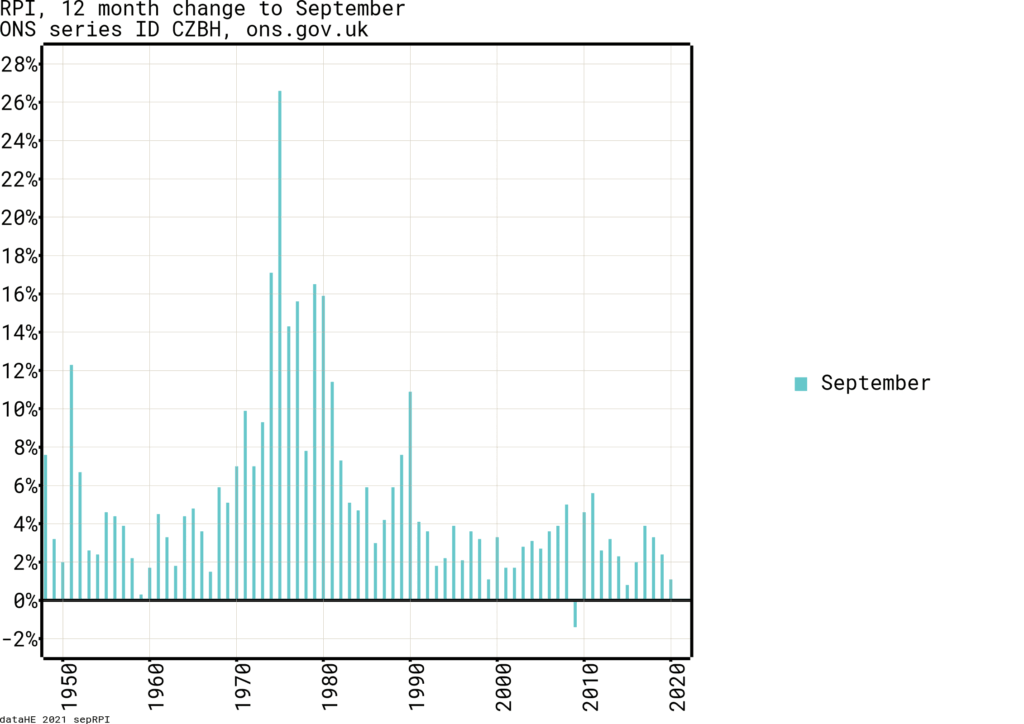

Figure 1 shows the change in prices measured by the RPI in the 12 months up to September over the past 70 years. In the past 30 years inflation has been modest, between one and five per cent. But this has not always been the case. Between 1970 and 1990 inflation was much higher, annual rates of over 10 per cent were common.

The pandemic has reminded us that modelling the future from just the recent past can be falsely reassuring. High inflation has happened before, so from a data perspective it is not unreasonable to assume it might happen again. For the purposes of this illustration September 2021 is set to be like September 1972 (RPI 7%), and the rest of the 2020s runs on from that point. Few, if any, economists currently expect that the 2020s would be like that. But it could happen, and the difficulties it highlights would be present, if attenuated, if inflation was below those levels but higher than recent years.

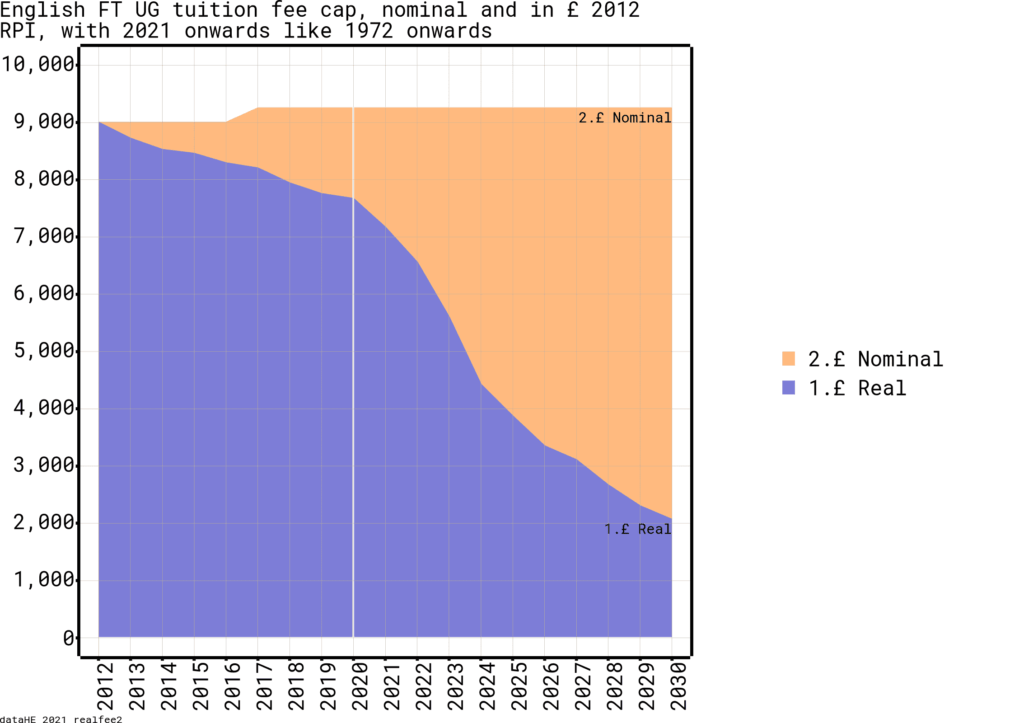

The cap for full-time undergraduate fees at universities in England was set at £9,000 for 2012 and increased once, in 2017, to £9,250. This is not the entirety of funds for teaching (for instance, there is additional government funding for certain high-cost subjects) but in England and Wales it dominates the resources universities have for teaching. Even the relatively low inflation over the past decade has been sufficient to erode the real value (in 2012 money) of that fee from £9,000 in 2012 to around £7,760 in 2020. Universities now have 15 per cent less to spend on teaching each student than they did in 2012.

If inflation were to follow a 1970s path, then the current financial model of universities unravels quickly. By 2022 real funding has fallen to £5,600, a 38 per cent cut from 2012. Two years later in 2024 the real value has slumped to £4,400, a 51 per cent cut. By this point universities are needing to teach two students with the resources they had for one in 2012. If universities made it through to 2030 in this scenario, they would find their real funding per student had dropped to around £2,000, less than a quarter of 2012 resource.

The other part of the 2012 arrangement that would be in uncharted territory with high inflation is the student loan system. Here the risk is of political acceptability.

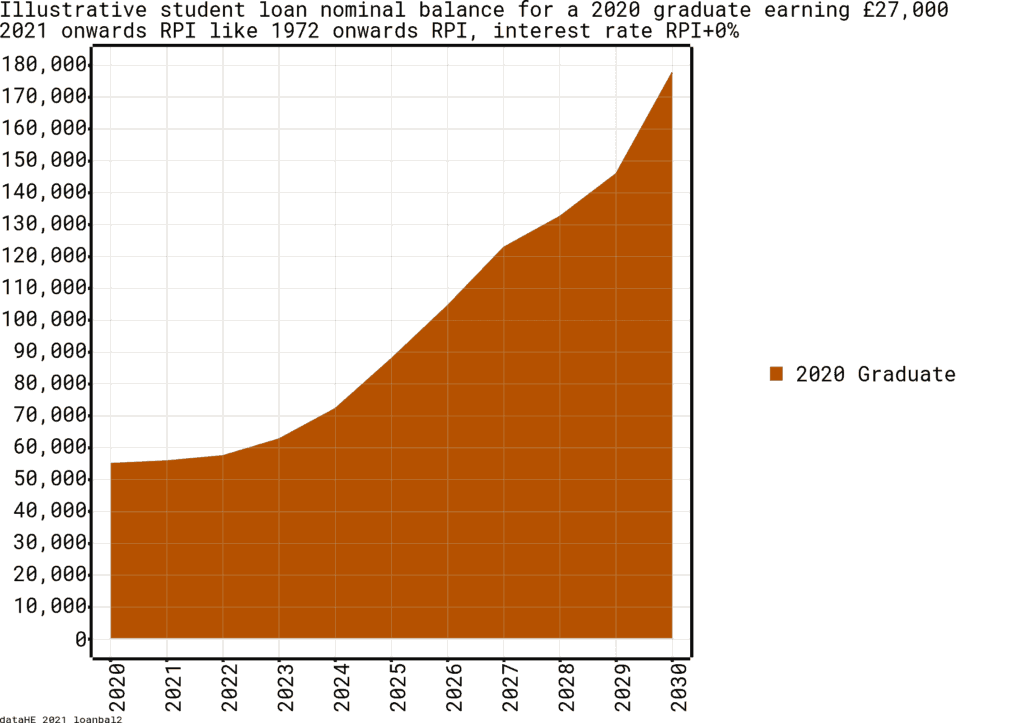

With loan support across three years for both fees and living costs it would not be unusual for 2020 graduate to have a loan balance of £55,000 or so. Somewhat in contrast to the funding for teaching, the government protects the real value of the money it is owed by applying an interest rate through a formula linked to inflation. For graduates with incomes below the threshold (just over £27,000 for 2021) the interest rate is just the RPI (determined from the previous March). For graduates above that threshold the interest rate varies by salary reaching RPI+3% for those earning around £50,000 or more. The DfE has the option to reduce the total interest rate if it is higher than comparable commercial loans (and indeed recently reduced interest by 0.3% under these provisions). But in a high inflation environment it is likely that the interest rates on commercial loans would also be high, so this provision is unlikely to aid students much.

In a high inflation world this indexing of the loan balance leads to some startling increases over time (Figure 3). Suppose our 2020 graduate spent the decade with an income below the threshold or was unemployed. By 2025 the outstanding loan balance would be almost £90,000, some 60 per cent higher than on graduation. By 2030 the graduate reading their statement would see that they owed almost £180,000, over three times their original balance.

Figure 3 Nominal student loan balance for a 2020 graduate.

The Government would, correctly, argue that the loan balance had not increased at all in real terms. And salaries would probably be increasing rapidly too. But the money illusion that works in the Government’s favour in terms of the fee cap, would now be working against it. It is likely that the public perception would be of graduates (including many making substantial repayments) falling deeper and deeper into debt due to a usurious government. With so many affected, political pressure might well follow. A rushed solution for graduates here, which would likely further increase the costs to government of higher education, could only be bad news for future student numbers and resourcing levels at universities.

The high inflation scenario is devastating because the current fee funding system for universities has an effective default of a fixed, rather than an indexed, fee. This leaves universities exposed to inflating costs, but unable to adjust income to compensate. Instead, they must rely on an active policy choice by government to increase the fee.

Politicians have learnt that increasing fee caps is both costly and wildly unpopular, in part because of the language and operation of student ‘debt’. The risk for universities is that this unappealing combination means governments hesitate far too long before increasing fees. In the meantime, universities are made threadbare, their teaching quality damaged in a way that cannot be quickly restored. The international standing of UK universities would likely decline.

Universities in Scotland and Northern Ireland, where direct grant funding is more important, are perhaps less susceptible to the political reluctance to raising student fees. There is also some direct grant funding to universities in England and Wales too (for example, for high-cost subjects) but it is relatively minor. Even where grants are important, high inflation still brings a risk of governments shying away from the annual nominal grant increases that would be needed to keep up with inflating costs. As things stand, there are few upsides for universities from high inflation, save for those that have been raising money through long-dated fixed-rate bonds.

The very high inflation future modelled here is perhaps unlikely. But it does serve to highlight tensions in the system that are with us today. Inflation only really becomes a problem because of the assumption that governments are predisposed not to help. The basis for this is that they seem to be increasingly questioning whether expanding numbers in university-level higher education is a good investment, and the sense that they would like to spend less, not more, on universities. This disposition is, in turn, probably influenced from their experience that the university tuition fee / debt system seems to give insufficient political return for the substantial public subsidy that (overall) students receive.

The best guard for universities against the risks of a high inflation world would be to address the these underlying tensions. Most importantly, finding a durable way to fund the growing demand for university education.

Comments

Add comment